Mark-to-Market: Settled Every Single Day

A futures position is settled in cash at the end of every trading day, not just at expiry. Learn how mark-to-market moves money in and out of your account daily and why a losing position can be closed for you.

- ·Daily cash settlement

- ·Profit and loss credited each day

- ·How MTM protects the exchange

- ·Margin top-ups

- ·Why you cannot ignore a position

- ·A two-day worked example

Imagine you and a friend make a bet on a cricket match, but instead of waiting until the last ball to settle up, you agree to pay each other at the end of every single over. If your team pulls ahead, money moves to you tonight. If it falls behind, you hand money over tonight. By the time the match ends, there is almost nothing left to settle, because you have been squaring accounts the whole way through. That, in one picture, is how a futures position works. It is not a quiet promise that sits untouched until expiry. It is settled in cash at the close of every trading day, and the money really moves in and out of your account.

This daily ritual is called mark-to-market, often shortened to MTM. It is one of the most important ideas in futures trading and one that beginners almost always underestimate. Once you understand that your open position is being valued and settled every evening, a lot of the mystery around margin, margin calls and overnight risk disappears.

What mark-to-market actually means

To mark to market is to revalue your position at the current market price and recognise the profit or loss right now, in cash, rather than waiting. The exchange takes the official closing price of the future, called the settlement price, compares it with the price your position was last valued at, and moves the difference between your account and the account of whoever is on the other side of your trade.

If the day went your way, the gain is credited to your margin account that evening. If the day went against you, the loss is debited from your margin account that same evening. There is no IOU, no waiting for expiry, no rounding off later. The cash is real and it has already left or entered your account by the next morning.

Two phrases describe the same idea, so keep both in mind:

- Daily settlement is the exchange process of paying out and collecting these differences at the end of each session.

- Mark-to-market profit or loss is the amount for your specific position, the gap between today's settlement price and yesterday's.

A futures position is settled in cash every trading day, not just at expiry. Your paper profit or loss becomes real money in your margin account at the close of each session.

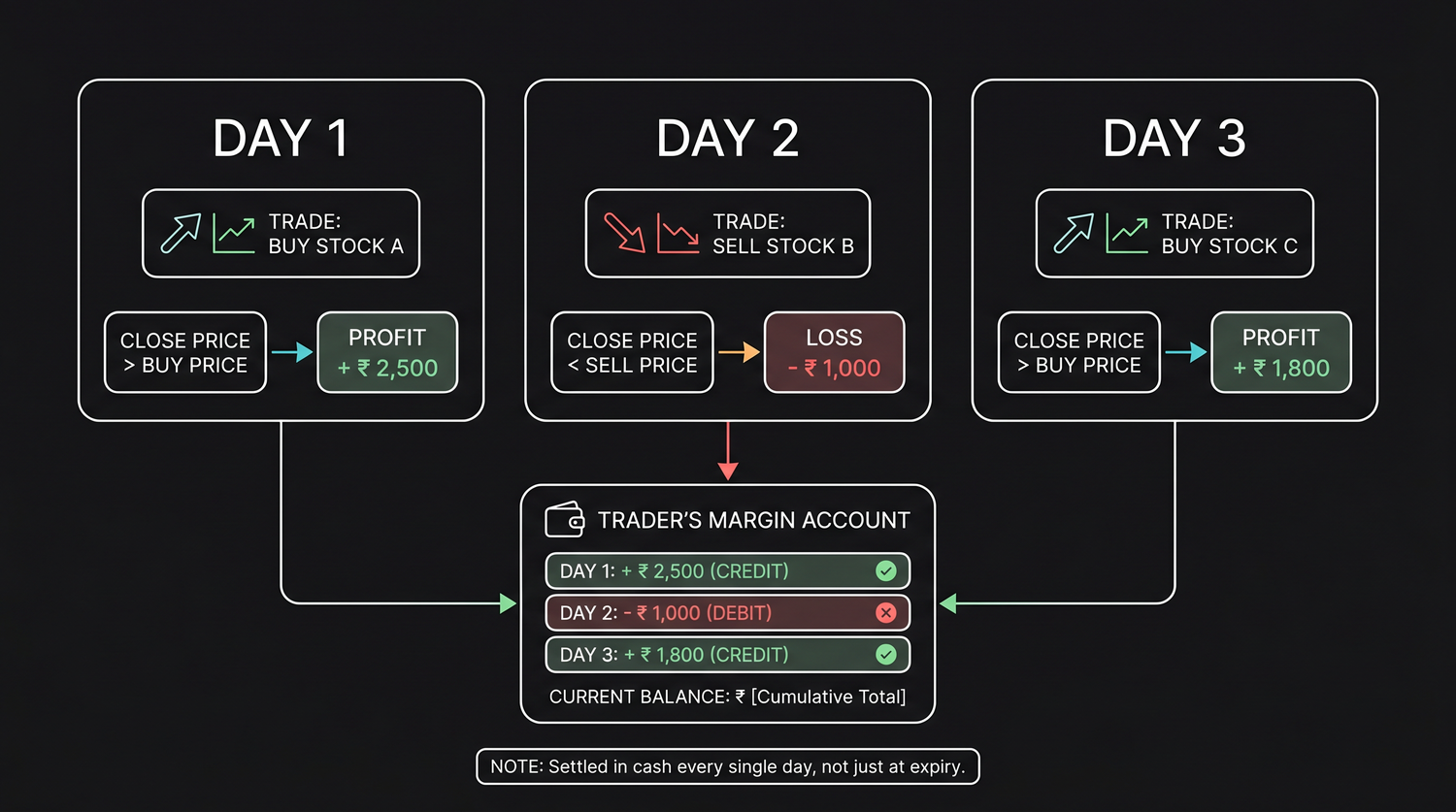

A two-day RELIANCE example

Numbers make this concrete, so let us trade one lot of the RELIANCE future. The lot size is 500 shares, and we will go long, meaning we buy first because we expect the price to rise. Suppose we enter at the round level of 1320.

The initial margin the exchange asks for is roughly Rs 1,30,000 to hold this one lot, so that is the cash sitting in our margin account on the day we enter. Now watch what happens over the next two trading days as the settlement price moves.

Day one closes at 1335. The future rose 15 points from our entry of 1320. Multiply by the lot of 500 shares and the gain is 15 times 500, which is Rs 7,500. That Rs 7,500 is credited to our account by the evening.

Day two closes at 1326. Notice the comparison is against yesterday's settlement of 1335, not our original entry. The future fell 9 points from 1335 to 1326. Multiply by 500 and the loss is 9 times 500, which is Rs 4,500. That Rs 4,500 is debited from our account that evening.

Here is the same story as a table.

| Day | Settlement price | Move vs previous close | Daily MTM (lot 500) | Margin account |

|---|---|---|---|---|

| Entry | 1320 | reference price | nil | Rs 1,30,000 |

| Day 1 | 1335 | up 15 points | plus Rs 7,500 | Rs 1,37,500 |

| Day 2 | 1326 | down 9 points | minus Rs 4,500 | Rs 1,33,000 |

After two days the future sits at 1326, which is 6 points above our entry of 1320. Six points times 500 shares is Rs 3,000, and sure enough the account has grown from Rs 1,30,000 to Rs 1,33,000, a net gain of exactly Rs 3,000. The daily settlements always add up to the total move. Mark-to-market does not change how much you make or lose in the end. It changes the timing, breaking one big settlement into many small daily ones.

On day one our long lot earned Rs 7,500 and the cash landed in the account that evening. We did not have to close the trade to collect it. Equally, the day-two loss of Rs 4,500 was taken out the same evening, whether we liked it or not.

Why the exchange insists on daily settlement

Mark-to-market can feel intrusive when a loss is pulled from your account overnight, but it exists to protect you as much as anyone. To see why, picture a world without it.

Suppose losses piled up silently for a month and were only collected at expiry. A trader on the losing side could rack up a loss far larger than the cash they ever deposited, then simply walk away and refuse to pay. The person on the winning side would be left holding a profit that exists only on paper, with no one able to honour it. The whole market would rest on trust, and trust breaks.

Daily settlement removes that danger by never letting losses grow unnoticed. Every evening, accounts are squared. Small losses are collected before they can snowball into amounts a trader cannot pay. This is how the exchange and its clearing corporation guarantee that the winner always gets paid.

- It caps how much credit risk can build up to a single day's move.

- It forces traders to keep enough cash in their account to back their position.

- It means the person on the other side of your trade is always made whole, because the exchange stands in the middle.

The body that performs this daily settlement and guarantees both sides is the clearing corporation. You never deal with it directly, but it is the reason a stranger on the other side of your trade can never leave you unpaid.

Margin top-ups and the margin call

Daily settlement links straight to margin. Recall that you posted an initial margin to open the position. As mark-to-market losses are debited evening after evening, that cushion shrinks. The exchange sets a lower threshold called the maintenance margin. If your account balance falls below it, you receive a demand to add cash back, and that demand is the margin call.

Continuing our example, imagine RELIANCE keeps falling instead of recovering. Each evening another loss is debited. Day three takes the future to 1300, a 26 point drop from day two's 1326, which is a loss of 26 times 500, or Rs 13,000. The account, already at Rs 1,33,000, drops to Rs 1,20,000. A few more red days like that and the balance slips under the maintenance level. At that point the broker asks you to top up the margin, often by the next morning.

If you do not add the cash, the broker is entitled to close your position for you, locking in the loss whether you wanted to exit or not. This is not the broker being harsh. It is the same daily settlement logic protecting everyone from a trader who can no longer fund their position.

A margin call is not optional. If you cannot or do not add funds in time, your position can be squared off by the broker at the worst possible moment. Always keep spare cash beyond the bare minimum margin so a few bad days cannot force you out.

Why you can never ignore an open position

The deepest lesson of mark-to-market is that a futures position is alive. It is not a certificate you tuck away and forget. Every trading day it is revalued, and real money moves. This is very different from owning a share, which can sit in your account for years while you ignore it, with the loss staying on paper until you choose to sell.

A futures position will not wait politely. A run of losing days quietly drains your margin, and if you are not watching, a margin call or a forced exit can arrive while your attention is elsewhere. The flip side is just as true. Profits are handed to you in cash daily, which is part of what makes futures attractive to active traders.

- Check your open positions and margin balance every single trading day.

- Keep a buffer of cash so a normal losing streak does not trigger a margin call.

- Remember that the settlement price, not the price you happened to see during the day, decides the evening's cash movement.

Before you ever take a real futures position, watch how mark-to-market behaves in sandbox trading (analyzer mode in OpenAlgo). Seeing the daily credits and debits without risking money makes the rhythm of daily settlement obvious.

Mark-to-market is the heartbeat of the futures market. It values your position every evening, moves real cash, protects the exchange from default, and demands that you stay awake to an open trade. Master this rhythm and the rest of futures trading, from margin to leverage, starts to make sense.