Hedging a Portfolio: Worked Examples

The original job of a future. Learn how shorting an index future protects a portfolio, with worked cases: a full hedge, a partial hedge, a high-beta portfolio, and what happens when the hedge size is wrong.

- ·What a hedge does

- ·Beta and the hedge ratio

- ·A full hedge worked through

- ·A partial hedge

- ·Hedging a high-beta portfolio

- ·When the hedge size is wrong

Imagine you have spent years building a portfolio of shares you believe in. RELIANCE, a couple of banks, an information technology name, a consumer company. You are happy to own them for the long run. But you read the news and you grow nervous. Maybe a budget is coming, or a global wobble, and you suspect the whole market could drop ten percent over the next month. You do not want to sell your shares, because selling means tax, costs, and the risk of buying back higher. Yet you do not want to sit and watch a tenth of your wealth evaporate either. There is a third option, and it is the reason futures were invented in the first place. You can hedge.

Hedging is using a futures position to protect something you already own from a fall in price. It is the original, sober purpose of the futures market, older than all the speculation, and understanding it will change how you see the whole instrument. A future is not only a way to bet. It is also a way to buy protection.

The original job of a future

Long before traders used futures to speculate, producers and owners used them to remove risk they did not want. A farmer who feared a price drop before harvest could lock in a selling price today. A mill that feared a price rise could lock in a buying price. Each one passed a risk they did not want onto someone willing to carry it. That is hedging, and it is still the purest use of a future.

For a modern investor the same logic applies. You own a basket of shares. You are exposed to the market falling. A hedge is a second position, deliberately set up to gain when your shares lose, so the two roughly cancel. You are not trying to make money on the hedge. You are trying to make the painful outcome less painful.

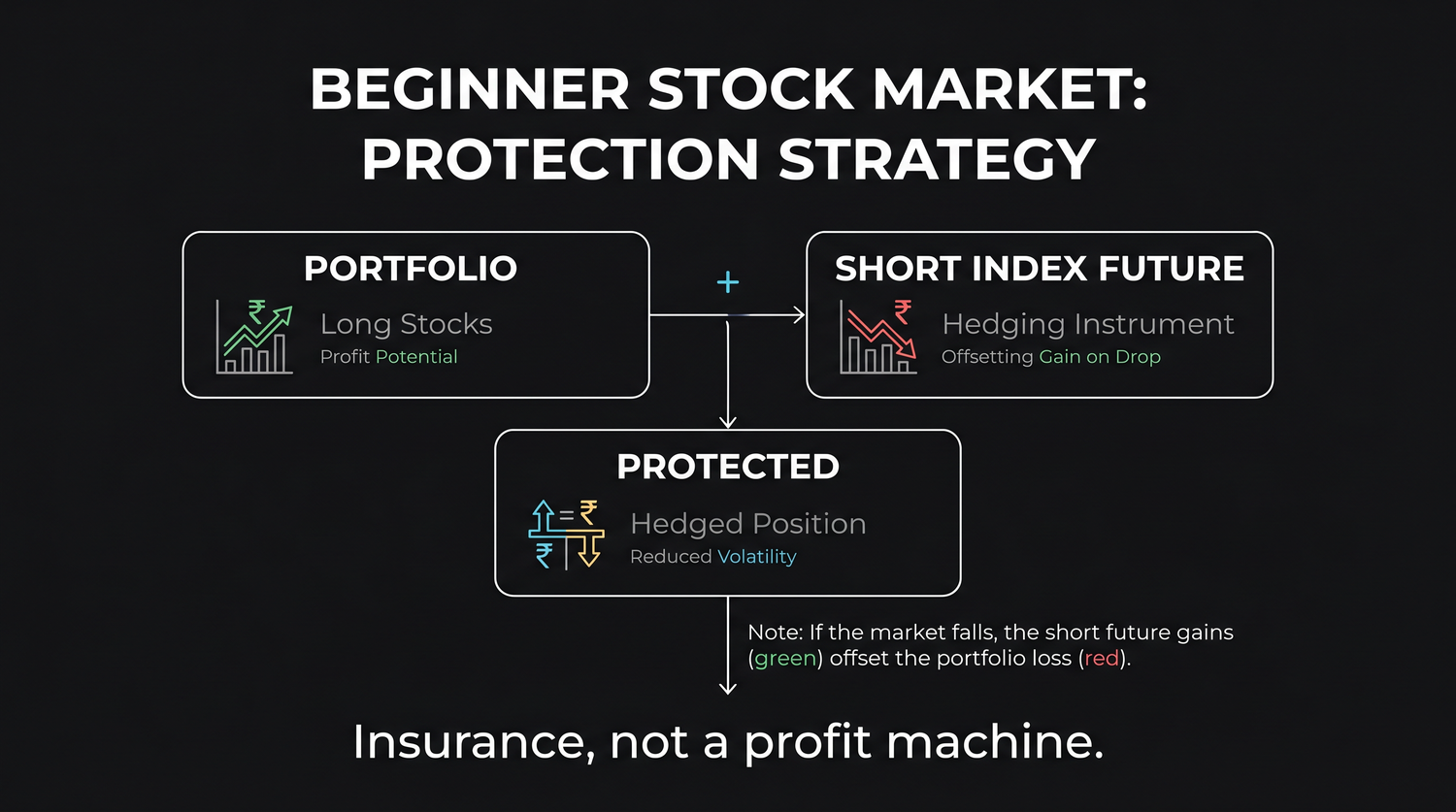

A hedge is a futures position taken to offset the risk in something you already own. When your holdings fall, the hedge gains, softening the blow. Its job is protection, not profit.

Shorting an index future to protect a portfolio

The most common hedge for a share portfolio is to go short an index future. Recall from earlier chapters that going short means you profit when the price falls. If you sell a NIFTY future and the market drops, that short position gains. If your diversified portfolio also falls with the market, your shares lose at the same time. The gain on the short offsets the loss on the shares. That is the whole mechanism.

Why use an index future rather than shorting each stock? Because a diversified portfolio tends to move with the broad market, so one liquid index future can offset the market risk of the whole basket in a single trade. You do not need to short RELIANCE, then the banks, then the rest. You short one NIFTY future and you have covered the general market exposure of everything at once. The index is deeply liquid and cash-settled, which makes it the natural instrument for this job.

You hold a diversified portfolio worth about Rs 16,00,000. Fearing a short term drop, you sell one NIFTY future. The market falls five percent over the next two weeks. Your shares lose roughly Rs 80,000 on paper, but your short NIFTY future gains a similar amount, so your total wealth barely moves. The hedge did its job.

Beta and how many lots to short

To size a hedge well you need one more idea, and it is simple in plain words. Beta measures how much your portfolio tends to move compared with the index. A beta of one means your portfolio moves about the same as NIFTY: if NIFTY falls ten percent, your portfolio falls about ten percent. A beta above one, say 1.3, means your portfolio is more jumpy than the index and tends to fall more. A beta below one, say 0.7, means it is calmer and tends to fall less.

Beta tells you how much index protection you actually need. A jumpy, high-beta portfolio needs a larger hedge than its plain rupee value suggests, because it falls harder than the index. A calm, low-beta portfolio needs a smaller hedge.

The hedge ratio is just the plain-language answer to one question: how many index lots roughly match the market risk of my holdings? You work it out in three steps, no formula required.

- Start with the total value of the portfolio you want to protect.

- Adjust it for beta: scale it up if your portfolio is jumpier than the index, down if it is calmer.

- Divide that adjusted value by the rupee value of one index futures contract to get the number of lots.

Put numbers to it. Suppose your portfolio is worth about Rs 15,60,000 with a beta near one, and NIFTY trades around 24,000, so one NIFTY lot of 65 controls about 24,000 times 65, which is roughly Rs 15,60,000. Your portfolio value and one contract's value are almost identical, and the beta is about one, so shorting a single NIFTY future hedges you well. If your portfolio were twice as large, you would short two lots. If its beta were 1.5, you would need more index exposure than the plain value suggests, so you might round up to the next lot.

Beta is just how much your portfolio moves relative to the index. The hedge ratio uses it to answer one practical question: how many index lots roughly offset my holdings? Higher beta means a larger hedge; lower beta means a smaller one.

A worked example: hedging a Rs 15,00,000 book

Let us make all of this concrete with real numbers, because a hedge stops feeling abstract the moment you watch it work. Suppose your holdings book is worth about Rs 15,00,000, spread across large, familiar shares, with a beta near one, so it tends to move roughly in step with the broad market. You are content to own every share for years, but a tense fortnight lies ahead and you want cover without selling.

First, work out how much index you actually need. NIFTY is trading near 24,000, and one NIFTY lot is 65 units, so a single contract carries about 24,000 times 65, which is roughly Rs 15,60,000 of exposure. Now run the hedge ratio in plain words: take the value you want to protect, which is Rs 15,00,000, scale it by your beta of about one, which leaves it near Rs 15,00,000, then divide by one contract's Rs 15,60,000. The answer is just under one lot. So shorting a single NIFTY future covers your book almost exactly, and you are nicely hedged with one clean trade.

Now play both outcomes forward over the next two weeks, because a hedge only makes sense once you see what it does in each direction.

If the market falls five percent, NIFTY slides about 1,200 points, from 24,000 to 22,800. Your portfolio, with a beta of one, loses about five percent of Rs 15,00,000, which is Rs 75,000. But your short NIFTY future gains 1,200 points times 65, which is about Rs 78,000. The two figures almost cancel, so your wealth barely flinches while the market drops. That is the protection you paid for, working exactly as designed.

If instead the market rises five percent, NIFTY climbs about 1,200 points to 25,200. Now your portfolio gains about Rs 75,000, which feels wonderful, but your short future loses about 1,200 points times 65, roughly Rs 78,000. Once again the two roughly cancel, and this time it stings: you handed back the rally. Here is the same story in one small table.

| Market moves 5% | Portfolio (beta 1) | Short one NIFTY future | Combined result |

|---|---|---|---|

| Falls to 22,800 | loses about Rs 75,000 | gains about Rs 78,000 | almost flat, you are protected |

| Rises to 25,200 | gains about Rs 75,000 | loses about Rs 78,000 | almost flat, you gave up the upside |

One short NIFTY lot against a Rs 15,00,000 book turns a five percent market swing, up or down, into almost no change in your wealth. That symmetry is the whole point. The hedge does not pick a direction; it simply removes the market's direction from your book for as long as it is on.

Notice what the future did and did not do. It did not earn you anything. It stood in for the fall you feared and, in all fairness, also gave back the rise you hoped for. That is why you should put a hedge on only when there is a reason worth the trade: a known event such as a budget or a result you cannot stomach, or a long holiday gap where the market reopens to digested global news and you cannot react in time. When there is no such trigger and you are content to ride the ordinary ups and downs of a market that drifts upward over the years, the cheapest and wisest hedge is usually none at all.

What the hedge costs you in a rally

Here is the part beginners often miss, and it is the honest centre of the whole idea. A hedge does not only protect you when the market falls. It also caps your gain when the market rises. The short index future that pays you in a drop will lose money in a rally, offsetting the rise in your shares. You have made your portfolio roughly market-neutral, which means you are protected on the downside and held back on the upside in equal measure.

Suppose, after you hedge, the market climbs five percent instead of falling. Your shares gain about Rs 80,000, which is lovely, but your short NIFTY future loses about the same, so your net gain is small. You gave up the rally in exchange for protection against the fall. There is no free lunch here. A hedge trades away some upside to remove some downside. That is exactly what insurance does.

There is also a small running cost. Holding the short index future carries the usual costs, and as you saw with the basis, a short position has its own relationship to the cost of carry. Over time, a permanent hedge quietly drags on returns, which is why hedges are usually temporary, put on for a specific worry and taken off when the worry passes.

A hedge is symmetrical. The same short future that cushions a fall will erase your gains in a rally. If you hedge and the market then climbs, do not feel cheated. You paid for protection and the protection cost you the upside, exactly as designed.

A hedge is insurance, not a profit machine

The cleanest way to hold all this in your head is to think of a hedge as insurance on your portfolio. You insure a house not because you expect it to burn but because you could not bear the loss if it did. The premium is money you are content to spend for peace of mind. A hedge works the same way. The upside you give up, and the small running cost, are the premium you pay to make a market drop survivable.

This framing also tells you what a hedge is not. It is not a way to make extra money. If you short an index future hoping to profit from a crash while keeping all your upside, you are no longer hedging, you are speculating with two positions. A true hedge accepts a capped upside as the price of a cushioned downside. Confusing the two is how people talk themselves into reckless trades and call them prudent.

When to hedge and when not to

Hedging is a tool, not a habit. Reaching for it constantly is expensive and pointless, because over the long run markets tend to rise and a permanent short bleeds your returns. Use it deliberately.

- Hedge when you face a specific, time-bound risk you genuinely fear: a major event, a result you cannot stomach, a market you think is stretched, and you want to ride through it without selling your holdings.

- Hedge when selling the underlying shares would be costly or undesirable for tax or long-term reasons, so a temporary future is cleaner than dumping and rebuying.

- Do not hedge permanently, because the capped upside and running cost will erode your returns over time.

- Do not hedge if you would honestly rather just reduce your position; sometimes selling some shares is simpler and cheaper than running a hedge.

Treat a hedge as a temporary umbrella, not a permanent roof. Put it on for a specific storm, size it with beta so it actually covers your portfolio, and take it off once the danger has passed. Left on forever, it quietly costs you the very growth you were trying to protect.

The enduring lesson is that the future began life as a shield, not a sword. By shorting a liquid index future against a portfolio you already own, you can blunt the pain of a market fall without selling a single share. Size it with beta, accept that it caps your upside as fairly as it cushions your downside, and remember at all times that a hedge is insurance. It is not meant to make you rich. It is meant to let you sleep.