Corporate Actions and F&O Adjustments

When a company splits its stock, issues a bonus or pays a special dividend, its futures and options are adjusted so open positions keep their value. Learn how a split or bonus changes the lot size and strike, how the adjustment factor works, the special-dividend threshold that triggers a change, and how rights and mergers are handled.

- ·Why F&O must be adjusted

- ·Splits and bonus issues

- ·The adjustment factor

- ·Lot size and strike changes

- ·Special dividends and the threshold

- ·Mergers and rights

One morning you open your trading screen and something looks wrong. Your RELIANCE position, the one you have watched all week, suddenly says the lot is 1000 shares, not the 500 you know by heart. The option you are sure you bought at the 1320 strike now reads 660. For a second your stomach drops. Did you lose half your money overnight? Did something break? The answer, happily, is no. Nothing went wrong. The company did something to its own shares, and the exchange quietly rewrote your contract so that your position is worth exactly what it was the day before. This is the world of corporate actions, and once you understand it a frightening surprise turns into a complete non-event.

What a corporate action does to a share

A corporate action is a deliberate decision by a company that changes its shares in some structural way. The ones a futures trader will meet most often are a stock split, a bonus issue, a rights issue, a special dividend, and a merger or demerger. Each of them, in its own way, changes either the price of a single share or the number of shares in existence, and sometimes both at once.

Take a stock split. A company whose shares trade near Rs 1,318 might decide the price is too high and split each share into two. Afterwards there are twice as many shares, and because the company is worth the same in total, each share is now worth about half as much, near Rs 659. Nothing about the business changed. The pie is the same size, simply cut into more slices. A bonus issue does much the same by another route. The company hands existing holders extra free shares, so the share count rises and the price per share falls to match. In both cases more shares exist and each one is individually cheaper.

Now hold any of these against an open futures or options position, and you can see the trouble coming.

The problem an open position faces

Imagine you are long one RELIANCE future. The lot is 500 shares and the future trades near 1320, so your position represents about Rs 6,60,000 of stock. Overnight the company splits its shares two for one, and the next morning the stock opens near 660, not because anything bad happened but purely because each share is now half of what it was.

If the exchange did nothing, your future, still defined as 500 shares, would now be worth only 500 times 660, which is Rs 3,30,000. Your position would appear to have lost half its value overnight, even though the business is unchanged and you did nothing wrong. The same cruelty would hit an option. A 1320 strike that was nicely in the money against a 1318 stock would suddenly tower far above a 660 stock and look worthless. The mechanics of the split, not any real move in value, would have wrecked your trade.

That is plainly unfair, and an exchange cannot allow it. A derivative is a promise written on top of the share. If the share is redefined beneath it, the promise must be rewritten to keep its meaning. Otherwise every split and bonus would hand a windfall to one side of each contract and an undeserved loss to the other.

A corporate action changes the share price or share count for reasons that have nothing to do with the company being worth more or less. If your contract were left untouched, that purely mechanical change would distort your position, making it look as though you gained or lost value when nothing real happened.

The principle: the exchange preserves value

Here is the idea that makes the whole chapter simple. When a corporate action hits a stock with futures and options on it, the exchange adjusts every open contract so the value of each position is preserved across the action. You are left holding something worth exactly what you held the moment before. Nobody gains and nobody loses from the mechanics of the adjustment itself.

This is the most reassuring fact in the chapter. The adjustment is not a trade, not a tax and not a fee. It is bookkeeping that keeps you whole. Your profit or loss is then measured from the adjusted position, so you neither pocket a windfall nor swallow a phantom loss from the split or bonus.

When a corporate action changes the underlying share, the exchange rescales the open futures and options contracts so the value of every position is exactly preserved. Nobody profits and nobody loses from the adjustment itself. It is a value-neutral rewrite, not a market move.

The adjustment factor

To rescale the contracts fairly, the exchange first works out a single number called the adjustment factor. In plain words it answers one question: how many of the new shares does one old share become?

For a two for one split, one old share becomes two new shares, so the adjustment factor is two. For a bonus where the company gives one free share for every share held, often written one to one, each old share effectively becomes two, so again the factor is two. The exchange publishes this factor for every adjustable corporate action, and everything else flows from it.

Once the factor is known, the rescaling is mechanical. The lot size is multiplied by the factor, because there are now more, cheaper shares per contract. The strike price of every option is divided by the same factor, because each share is individually cheaper. The futures price and your option premium are restated in the same proportion. Multiply one side up and divide the other down by the identical number, and the total value lands back where it started.

Splits and bonus issues: a worked example

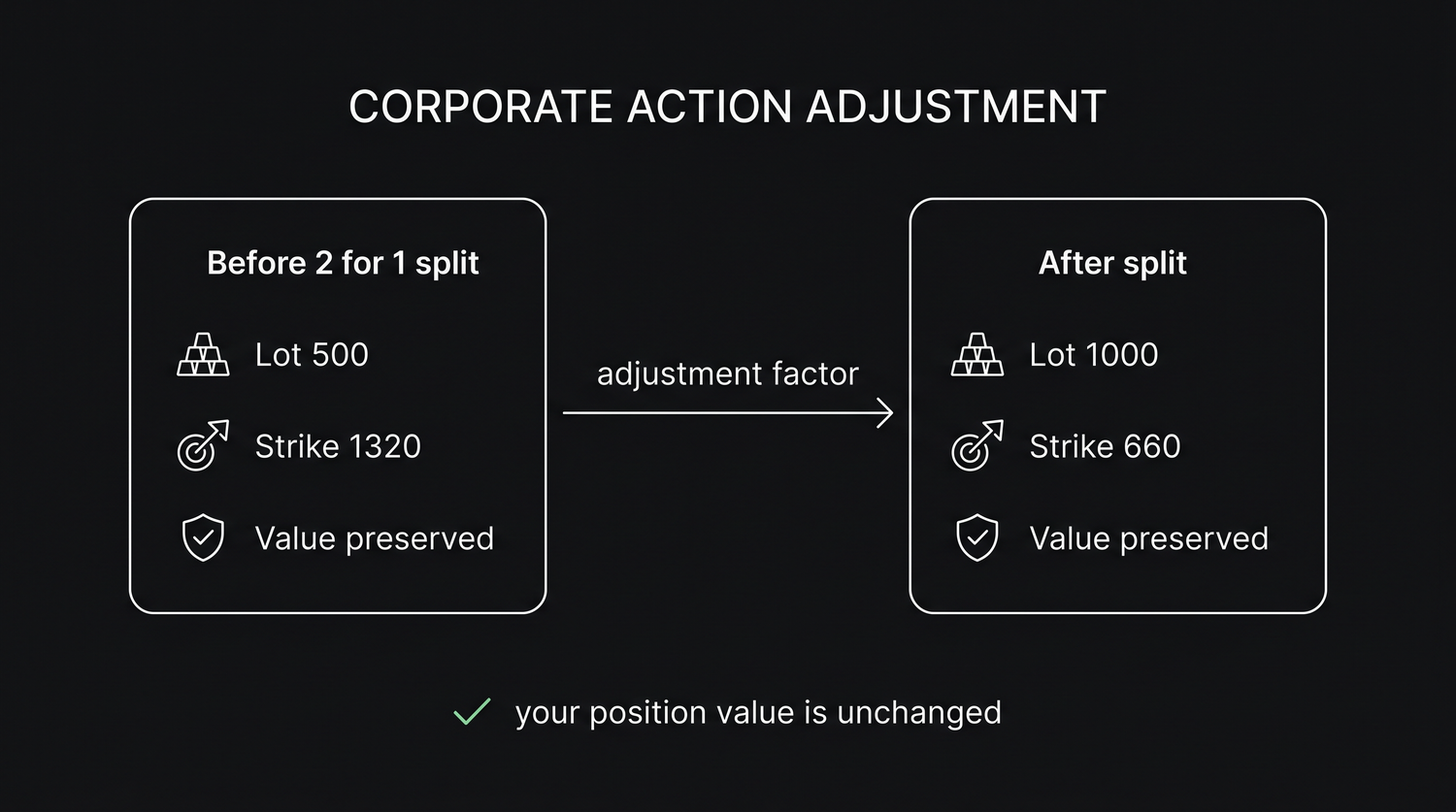

Let us walk the RELIANCE numbers through a two for one split, an adjustment factor of two.

| Before the split | After the split | |

|---|---|---|

| Share price | about Rs 1,320 | about Rs 660 |

| Lot size | 500 shares | 1000 shares |

| One futures lot value | about Rs 6,60,000 | about Rs 6,60,000 |

| An option strike | 1320 | 660 |

Notice what happened to the future. The lot doubled from 500 to 1000 and the price halved from about 1320 to about 660. Multiply them and you get the same roughly Rs 6,60,000 of exposure on both sides. Your one lot is still one lot, the same money at work, simply expressed as twice as many shares each worth half as much.

The option is just as clean. The 1320 strike becomes the 660 strike and the lot it controls grows from 500 to 1000. An option that was two rupees in the money against a 1318 stock becomes the 660 strike against a 659 stock, still about one rupee in the money per share across twice the shares. Its real worth did not move, only its labels did. A one to one bonus produces identical arithmetic, because it too doubles the share count and halves the price.

So why did your screen change overnight? Because the adjustment is tied to two dates the company announces. The record date is the day the company checks its share register to decide who is entitled to the split or bonus. The ex-date, usually set just before it, is the first day the stock trades without that entitlement attached, which is exactly when the price steps down to its new lower level. The exchange applies the contract adjustment from the ex-date, so the rescaled lot, the rescaled strike and the cheaper share price all appear together, and your position value carries across unbroken.

You hold one RELIANCE 1320 call before a two for one split. On the ex-date the stock opens near 660, your call is relisted as a 660 strike, and the lot behind it grows from 500 to 1000 shares. You did nothing, paid nothing and were charged nothing. The numbers on your screen changed, the worth behind them did not.

Special dividends

Dividends are the one case where the exchange usually does nothing. Companies pay ordinary dividends all the time, the stock dips by roughly the dividend on its ex-date, and because that small, expected drop is part of normal life, derivative contracts are left untouched. Adjusting for every routine payout would be needless churn.

The exception is a special dividend, an unusually large one off payment. When a dividend is big enough, the ex-date drop is no longer a small wobble but a real lurch that would distort open option positions much like a split. So the exchange sets a threshold, a percentage of the stock price, above which a dividend counts as extra-ordinary and does trigger an adjustment. Below the threshold, no change. Above it, the strikes are adjusted for the payout so option holders are not unfairly hurt by the drop.

The dividend threshold and the exact method are set by the exchange, not by you or your broker, and they have been revised before. Treat the percentage rule as the current framework rather than a fixed law, and confirm the figure in force against the latest NSE corporate-actions adjustment circular before you assume how a particular dividend will be treated.

Rights issues and mergers

The remaining corporate actions are handled with the same goal, value preserved, but they need more care because the maths is less tidy.

A rights issue lets existing shareholders buy new shares at a price below the market, which dilutes the value of each existing share. There is no single clean ratio like a split. The exchange computes an adjustment factor from the rights ratio and the discounted price, then rescales the lot and strikes by that factor in the same value-neutral way. The principle is unchanged. Only the number is harder to eyeball.

Mergers, amalgamations and demergers are handled case by case, because the underlying itself may be changing identity. Sometimes the contract is adjusted to reflect the new combined entity and trading continues. Sometimes, when a company is being absorbed and will cease to exist as a separate stock, its derivative contracts are settled at a fair value and discontinued, or transitioned into contracts on the surviving company. There is no universal recipe. For each event the exchange issues a specific circular spelling out precisely what happens to the open contracts, so the decision is never improvised.

What you actually need to do

For all the machinery, the practical instruction is short and calming. You do not need to do anything. You place no order, sign no form and pay no adjustment fee. The exchange rescales your contract automatically on the ex-date and your position carries across whole.

What you do owe yourself is understanding, so the morning your lot reads 1000 instead of 500 or your strike reads 660 instead of 1320, you recognise it instantly as a corporate-action adjustment rather than an error or a loss. Two habits make that effortless. First, glance at the corporate-action announcements for any stock you hold derivatives on, so a split, bonus or special dividend never ambushes you. Second, when something does look rescaled, check the exact treatment on the NSE corporate-actions adjustments page, where the factor and the method for that specific event are published. The thresholds and the precise methods are exchange-defined and can change, so the current circular, not memory, is the authority.

You never have to act on a corporate-action adjustment, but you should always understand it. If your lot size or strike suddenly looks different, do not panic and do not assume a glitch. Confirm it against the NSE corporate-actions adjustment circular for that stock, see the value preserved, and carry on.

The takeaway is gentle by the standards of this course. Most of futures trading is about danger you must defend against. Corporate actions are the rare case where the system works quietly in your favour, redrawing your contract so a split, bonus or special dividend cannot rob you of value or hand you an unearned gain. Know that it happens, know why your numbers change, and let the exchange do its bookkeeping while you watch the trade itself.