Futures vs Forwards, Options and Shares

A future is not a forward, not an option, and not a share. Learn how a standardised exchange-traded future differs from a private forward, why a future is an obligation while an option is a right, and why holding a future is not the same as owning the stock.

- ·Standardised future vs private forward

- ·Exchange-traded and guaranteed

- ·Obligation vs an option's right

- ·A future is not owning the share

- ·No dividends, no votes

- ·Why the difference matters for risk

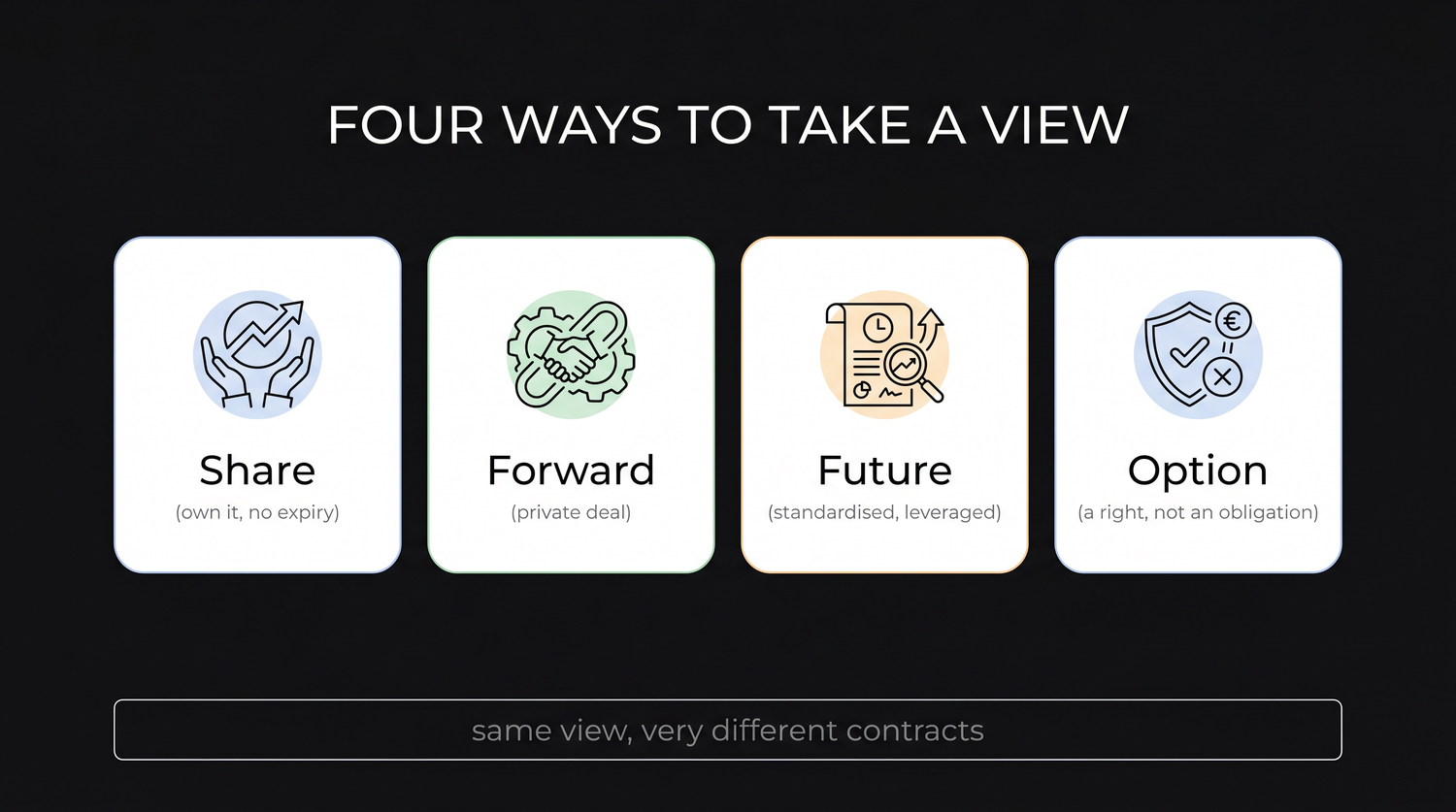

When you walk into a market to put money on RELIANCE, you are not handed a single tool. You are handed a small family of them, and they look alike from a distance but behave very differently once money is on the line. You can buy the shares and become a part owner of the company. You can buy a future and lock a price with an obligation attached. You can buy an option and pay for the right to change your mind. Each is a real, sensible choice for a real, sensible reason, and the worst mistakes beginners make come from picking the wrong one of these four without realising the others existed. So before we go deeper into futures, let us place a future among its cousins and see exactly what you are choosing when you choose it.

The four instruments we will compare are the forward, the future, the option, and plain cash equity, which simply means owning the share outright. They sit on a spectrum from the most informal handshake to the most formal, exchange-policed contract, and from pure ownership to a pure timed bet.

The forward: a private, custom handshake

Remember the baker and the farmer from the first chapter. They sat down, agreed a price for wheat to be delivered in two months, and shook hands. That deal is a forward contract, and it is the oldest member of this family. A forward is a private agreement between two parties to trade something at a fixed price on a fixed future date. Nothing about it is standardised. The baker and farmer can pick any quantity, any quality of wheat, any delivery date, any price they both accept. That flexibility is genuinely useful, because the deal can be shaped to fit exactly what each side needs.

But the flexibility comes at a steep cost, and the cost has a name: counterparty risk. A forward is only as good as the person on the other side of it. If wheat prices crash and the farmer would rather sell to someone else at the higher market rate, what stops him from quietly walking away? Only the baker's ability to chase him through the courts. There is no referee standing between them. If one side cannot pay or simply refuses, the other is left holding a broken promise. A forward is also illiquid. Because it was custom-built for two specific people, the baker cannot easily sell his side of the deal to a stranger halfway through. He is stuck in it until the delivery date.

A forward is a private, negotiated, one-off deal. It is wonderfully flexible because the two parties write their own terms, but it is illiquid and it carries counterparty risk, the danger that the other side simply fails to honour the agreement.

The future: the forward, cleaned up and policed

A future is what you get when you take that same forward idea and run it through an exchange. The exchange does two transforming things to it.

First, it standardises the contract. Instead of a custom quantity, you trade in fixed lots, 500 shares for a RELIANCE future. Instead of any date you like, you trade fixed expiries, the last Tuesday of the month, such as 28 July 2026 for our worked contract. Because every RELIANCE future is identical to every other, thousands of buyers and sellers can trade the very same contract. That is what makes a future liquid: you can enter today and exit in seconds tomorrow by trading the offsetting contract, something the baker could never do with his handshake.

Second, and more importantly, the exchange's clearing house steps into the middle of every trade. When you buy a RELIANCE future, you are not really relying on the specific person who sold it to you. The clearing house becomes the buyer to every seller and the seller to every buyer. It guarantees the deal. To make that promise safe, it collects margin from both sides and settles profit and loss in cash every single day, an idea we devote a whole later chapter to. The result is that counterparty risk all but disappears. You never have to wonder whether the stranger on the other side is good for the money, because the clearing house is standing behind it.

A future is simply a forward that has been standardised and exchange-traded, with a clearing house in the middle that guarantees both sides and removes counterparty risk. You give up the forward's custom flexibility and gain liquidity and safety in return.

The option: a right, not an obligation

The option is the cousin that behaves in a genuinely different way, and the difference is one word: choice. A future is an obligation. If you are long a RELIANCE future, you are bound to it, and if the price falls you carry the full loss with no escape. An option flips this. The buyer of an option pays a fee, called the premium, for the right but not the obligation to buy or sell at a set price. If the trade goes their way they exercise the right. If it goes against them, they simply let the option lapse and lose nothing more than the premium they already paid.

That single difference bends the entire shape of the payoff. A future's payoff is a straight line: every Rs 1 that RELIANCE moves is Rs 500 to your one-lot position, up or down, perfectly symmetric, an idea we explore in full in a later chapter. An option's payoff is not a straight line. It bends, because the buyer's loss is capped at the premium while the gain can keep growing. The buyer has bought the right to walk away from the bad outcomes, and that asymmetry is what they pay the premium for. A future holder has no such mercy and pays no such premium.

The defining difference is obligation. An option buyer can walk away and lose only the premium, so the payoff bends and the downside is capped. A future holder is locked in, so the payoff is a straight line and the loss can be very large. Never confuse the two.

Cash equity: actually owning the business

Last comes the most familiar instrument of all, and the one that is not a derivative at all. When you buy cash equity, you simply buy the share. You pay the full price, all of it, and you become a part owner of the company. There is no expiry date hanging over you. You can hold the share for a day or for thirty years. Because you own a real slice of the business, you receive dividends when the company pays them and you get voting rights in company decisions. None of the other three give you that.

The trade-off is that cash equity has no built-in leverage. To control Rs 6,59,000 of RELIANCE through shares, you pay the whole Rs 6,59,000, not a small margin. You can borrow to amplify it, but that is a separate loan you arrange, not a feature of the instrument itself. Owning shares is the calmest, most patient member of the family. There is no daily settlement to watch, no contract to roll, no clock ticking down. You own the business and you wait.

The four side by side

Here is the whole family in one view. Read it across each row and the personality of each instrument becomes obvious.

| Feature | Forward | Future | Option | Cash equity |

|---|---|---|---|---|

| Ownership | None, just a promise | None, a contract | None, a right | Full ownership of the share |

| Expiry | A fixed date you both choose | A fixed exchange date | A fixed exchange date | None, hold forever |

| Leverage | By private agreement | Built in, post only margin | Built in, pay only premium | None unless you borrow |

| Obligation | Both sides obliged | Both sides obliged | Buyer chooses, seller obliged | None |

| Settlement | Privately, at the end | Daily, by the clearing house | At exercise or expiry | At purchase, once |

| Counterparty risk | High, no guarantor | Removed by clearing house | Removed by clearing house | None, you hold the share |

| Who uses it | Two businesses with a custom need | Traders wanting capital-efficient direction | Traders wanting defined-risk bets | Long-term owners and investors |

So which one should a beginner pick?

The honest answer is that the right tool depends entirely on what you are actually trying to do, and naming your real goal is half the battle.

If you want to own a business and share in its long-term growth, collect its dividends and have a vote, you buy the shares. There is no expiry to fight, no daily settlement, no leverage to blow you up. This is where most people should start and where most wealth is quietly built.

If you want a defined-risk bet, where you know in advance the very worst that can happen to you, you buy an option. Your maximum loss as a buyer is the premium, decided before you enter, and that capped downside is exactly what you are paying for.

If you want a pure, capital-efficient directional position on a liquid underlying, you use a future. You post only a margin rather than the full Rs 6,59,000, so a single RELIANCE lot or one NIFTY lot of 65 near 24,000 gives you full exposure for a fraction of the cash. In return you accept two things squarely: the obligation, which means there is no walking away from a loss, and the daily settlement, which means the position is marked against you in cash every day. The forward, meanwhile, is really a tool for businesses with a specific custom need, not for a screen trader, because you simply trade its cleaner cousin, the future, instead.

Before you place any trade, say out loud what you actually want: to own a business, to make a capped-risk bet, or to take a leveraged directional view. The answer points straight at shares, an option, or a future. Most costly mistakes start with reaching for the wrong instrument.

You now know where a future sits in its family and what you accept when you choose it. In the next chapter we meet the two kinds of people who keep this market alive, the hedger who wants to shed a risk and the speculator who is happy to take it on, and we see why neither could function without the other.