SPAN Margin, Exposure and Pledged Collateral

Margin is not a fixed number. Learn how it is built from SPAN plus exposure, why it rises when volatility rises, what peak-margin rules mean, and how Indian traders pledge holdings as collateral, including why margin available is not the same as free cash.

- ·SPAN plus exposure margin

- ·Why margin changes dynamically

- ·Volatility-driven margin hikes

- ·Peak margin and blocking

- ·Pledging collateral vs cash

- ·Why collateral is not free cash

You opened a RELIANCE future yesterday with a comfortable cushion of free cash sitting behind it. This morning, before you have placed a single new order, your broker tells you the same position now needs more money to stay open. You have done nothing. The stock has barely moved. Yet the deposit demanded against your trade has quietly grown overnight. This is not a glitch and it is not unfair. It is the margin system doing exactly what it was built to do, and understanding it is the difference between a trader who is never caught short and one who is forced out at the worst possible moment. An earlier chapter introduced the deposit and the leverage it creates. This chapter goes underneath the number to show how it is built, why it changes, and how you can back it with shares instead of pure cash.

A quick recap: SPAN plus exposure

You already met the two pieces that make up a futures margin, so we will be brief and then build past them.

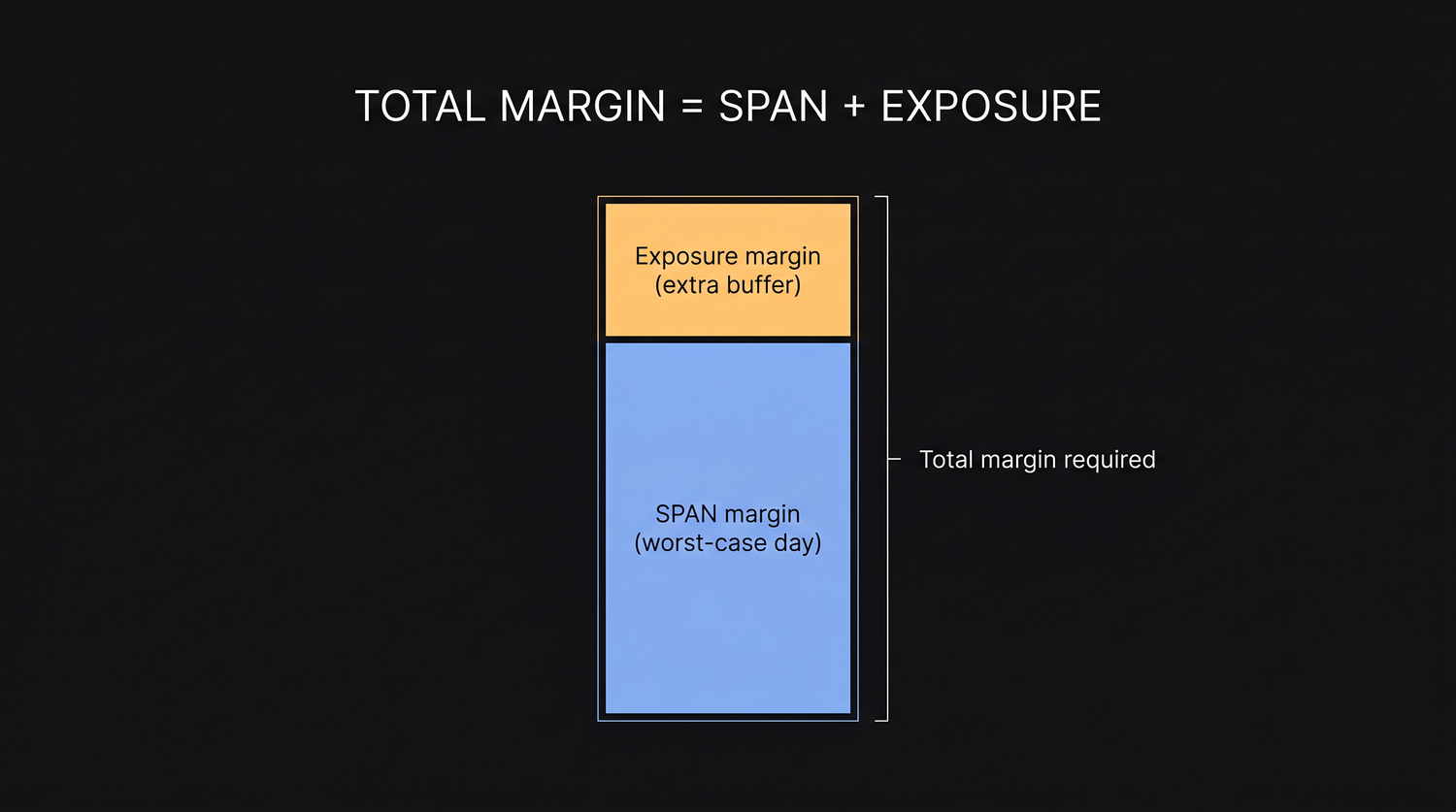

The bulk of your deposit is SPAN margin. SPAN is the exchange's risk engine, and this part is the amount it judges necessary to cover the worst-case loss your position could suffer in a single trading day. It models a whole range of price and volatility moves and takes the most punishing plausible one. On top of that sits the exposure margin, a smaller extra buffer the exchange adds for protection against a move even more violent than the worst case SPAN modelled. Neither part is optional, and added together they give the total margin required, the actual cash that must sit free in your account before the order will go through.

For one RELIANCE lot, controlling about Rs 6,59,000 of stock, that total lands somewhere near Rs 1,10,000, most of it SPAN with a thinner slice of exposure on top. For one NIFTY lot of 65 near 24,000 the structure is identical, just different numbers.

SPAN is the worst-case one-day risk and forms the bulk of your deposit. Exposure is the extra buffer stacked above it. SPAN plus exposure equals the total margin you must post, and that single number is what the OpenAlgo margin calculator hands you before a trade.

Margins are not fixed

Here is the idea most beginners never see coming, and it is the heart of this chapter. The margin on a contract is not a fixed number. It is recalculated, and the exchange can raise it whenever it decides the risk has grown.

Remember what SPAN is measuring: the worst plausible one-day loss. When a stock or an index becomes more volatile, its plausible one-day move gets larger, so the worst-case loss gets larger, so the margin required to cover it climbs in step. A calm market carries a leaner margin. A jumpy, frightened market carries a fatter one. The deposit breathes with the volatility of the underlying.

The exchange also raises margins ahead of known events. Before a national budget, a central bank rate decision, a general election result, or a company's earnings, everyone can see that a big move is possible. The exchange does not wait to be surprised. It lifts margins in advance so that every open position is better cushioned before the event lands. This is why a position you opened in a quiet week can suddenly demand noticeably more cash the night before a major announcement, even though the price has not moved at all.

The practical sting is the timing. A margin hike arrives precisely when the market is nervous, which is precisely when your own position may already be under pressure. If your account is funded right up to the edge, an overnight increase can tip you into a shortfall and force you to add money fast or trim the position. The trader who left a buffer simply absorbs it and sleeps.

A comfortable margin today is not a guarantee of a comfortable margin tomorrow. The exchange can raise the requirement overnight when volatility rises or a big event approaches, so a position funded to the very edge can fall short without the price moving a single rupee against you.

The expiry-week spike on stock futures

There is one more margin increase, and it is large, scheduled, and unique to single-stock futures like RELIANCE. As the contract approaches its final days, the exchange begins to ramp the margin up sharply through the physical-settlement week.

The reason is that a stock future, unlike an index future, can end in actual delivery of shares. If you are still holding a RELIANCE future when it expires, you may be obliged to give or take 500 real shares, which needs far more than the slim margin that let you hold the bet. To make sure nobody drifts into delivery by accident with too little money behind them, the exchange steadily increases the margin across the expiry week, pushing it toward the full contract value for anyone who has not yet closed out.

We give physical settlement its own full chapter later, so for now just hold the warning. A stock future that was cheap to carry all month can become very expensive to hold in its final days, purely because of this scheduled spike. A beginner who only ever wanted a leveraged directional bet should close or roll a stock future before that week arrives, rather than be surprised by a margin demand that suddenly multiplies.

Index futures such as NIFTY and BANKNIFTY settle in cash and carry no delivery, so they do not see this expiry-week spike. The sharp ramp in the final days is a stock-future feature, driven by the threat of physical delivery, and it is one more reason beginners often prefer the index.

Collateral and pledging: backing margin with holdings

So far we have spoken as if margin must be cash. It does not all have to be. If you already own shares, exchange-traded funds, or government bonds, you can put them to work as collateral instead of leaving large sums idle in cash. The mechanism is called pledging.

When you pledge a holding, you do not sell it. You formally mark it as security against your trading account, and in return the broker credits you a collateral margin that you can use to meet the margin on your futures positions. Your shares stay yours, you keep their long-term upside and any dividends, and the same capital is now doing two jobs at once.

There is a catch, and it is important. You do not get margin equal to the full market value of what you pledge. The system applies a haircut, a deliberate reduction, before crediting you. If you pledge shares worth Rs 1,00,000 and the haircut is, say, around 15 percent, you receive roughly Rs 85,000 of usable margin, not the full lakh. The haircut exists because the pledged shares themselves can fall in value, so the exchange keeps a margin of safety between what the holding is worth and what it will lend you against it. A steadier holding like a large index fund or a government bond carries a smaller haircut. A volatile single stock carries a larger one.

The cash component rule

This brings us to the rule that stops pledging from becoming a free lunch. You can never run a futures account on pledged shares alone. The exchange enforces a cash component, meaning a minimum portion of your total margin, broadly around half, must be met with actual cash or cash-equivalent instruments such as liquid funds, not with pledged equity.

The logic follows directly from mark-to-market. Your daily losses are debited in real cash, every single day. Pledged shares cannot be shaved a little each evening to pay a loss, so the exchange insists that a solid cash base is always present to settle those daily debits. If your cash portion runs too thin relative to your pledged collateral, the broker can charge interest on the shortfall or refuse new positions until you restore the balance.

So pledging is best understood as a way to make idle holdings useful, not as a way to escape needing cash. A realistic futures account holds a healthy cash balance to cover daily settlement and margin hikes, and uses pledged collateral to extend its capacity beyond that base, never to replace it.

Treat pledged shares as a supplement to cash, never a substitute. Plan for roughly half your margin to be real cash because daily losses are settled in cash, and keep a spare cash cushion on top so a margin hike or a run of losing days does not force you to unpledge and sell at a bad time.

Putting it to work before every trade

The threads of this chapter tie into one simple habit. Before you place a futures order, open the OpenAlgo margin calculator, enter the exact contract, side, and quantity, and read off the SPAN, the exposure, and the total margin required as they stand right now. That number already reflects today's volatility and any event-driven increase, so it tells you the truth about what the position costs to carry at this moment, not what it cost last week.

Then fund it with deliberate slack. Do not match your free capital to the margin exactly, because the margin can rise overnight, the expiry week can ramp a stock future sharply, and your daily losses come out in cash. A trader who keeps a genuine cash buffer behind every position absorbs all three without drama. A trader funded to the last rupee meets each of them as an emergency.

Most leveraged futures traders lose money, and being forced out by a margin shortfall rather than by a considered exit is one of the common ways it happens. The cure is unglamorous. Check the calculator every time, keep cash in reserve for hikes, and never confuse the margin you can scrape together today with the margin the exchange may demand tomorrow.

The takeaway is short. SPAN plus exposure is the deposit, but that deposit is a moving target that the exchange lifts when volatility climbs, before big events, and through a stock future's expiry week. You can back part of it by pledging shares, ETFs, or bonds, accepting a haircut for the privilege, but the cash component rule means real money must always sit underneath. Respect the moving number, keep cash in hand, and the margin system becomes a manageable cost of doing business rather than the thing that ends your run.