Roll Spreads, Calendar Spreads and Basis Trading

The gap between two months and the gap between future and spot can themselves be traded. Learn the roll spread you pay at rollover, the calendar spread as a position, and the idea of cash-futures arbitrage, which you should understand but not blindly attempt.

- ·Near-month vs next-month pricing

- ·The roll spread you pay

- ·The calendar spread position

- ·Fair value and the basis

- ·Cash-futures arbitrage explained

- ·Why retail should not chase it

Every price you trade was set by someone. When you buy a RELIANCE future a few points above the share, that premium did not appear by accident. A professional desk somewhere has already weighed the cost of holding the stock to expiry and decided that gap is fair, and if it ever drifts too far from fair, that same desk steps in and trades it back. This chapter lifts the lid on what those professionals actually do with the carry you met in earlier chapters. It is the most advanced material in the course, and you may never place these trades yourself. But understanding them tells you who sets the prices you trade against, and why a future can never wander far from the share it tracks.

We will look at two professional moves. The first is the calendar spread, where you trade the gap between two expiry months instead of the direction of the market. The second is basis trading, the cash-futures arbitrage that quietly tethers every future to its fair value. Both grow straight out of the cost of carry, so keep that idea from the basis chapter close at hand.

Trading the spread, not the direction

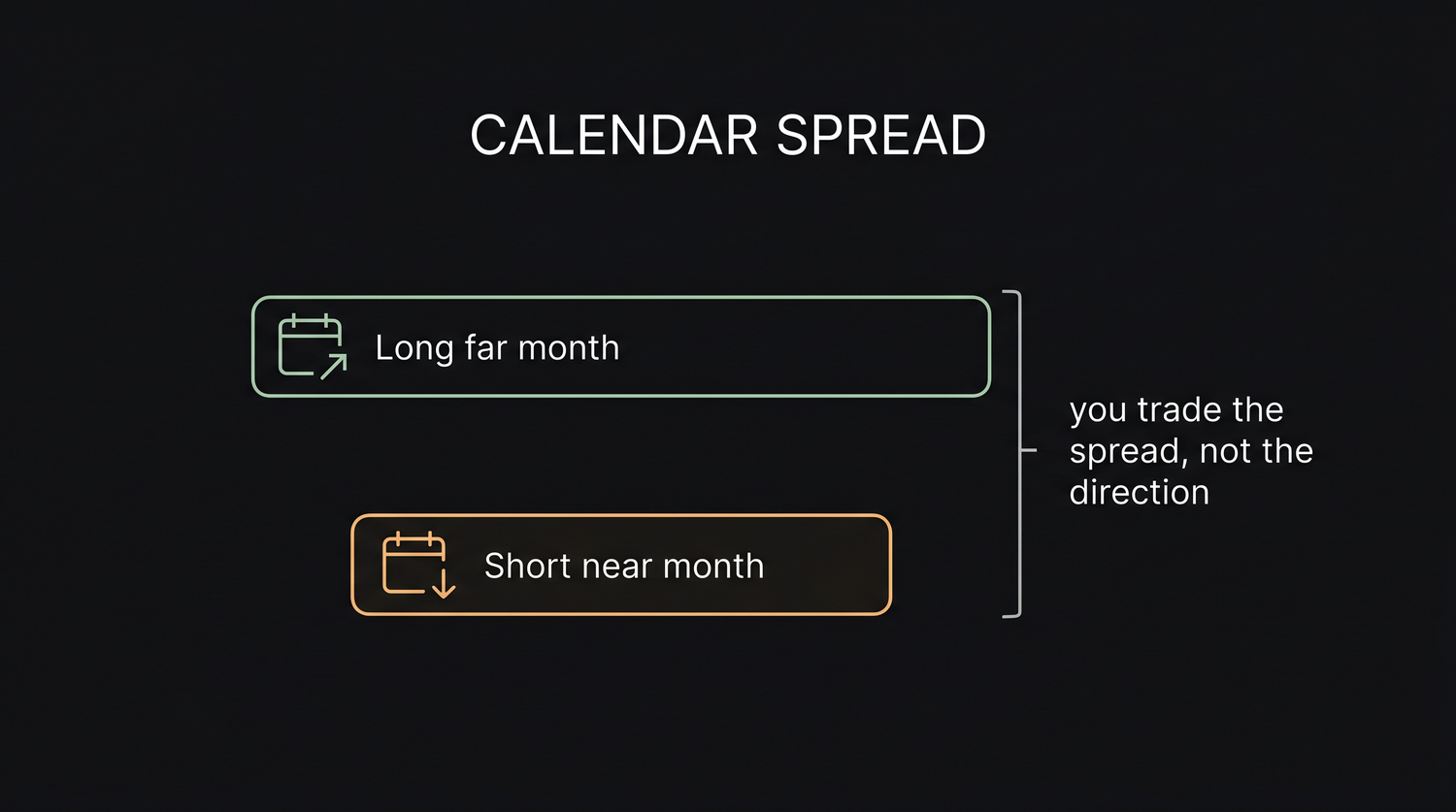

Until now every position you have studied has had a direction. Go long and you profit if the price rises. Go short and you profit if it falls. A calendar spread is different, and the difference is what makes it advanced.

A calendar spread means being long one expiry and short another expiry of the very same underlying at the same time. You might buy one lot of the RELIANCE August future and sell one lot of the RELIANCE July future. Notice what you now own. You are long RELIANCE in one month and short RELIANCE in another month. If RELIANCE as a company rallies hard, both legs move together, the long gains and the short loses by almost the same amount, and the two cancel. If RELIANCE collapses, again both legs move together and again they roughly cancel. You have stripped the direction of the stock out of the position almost entirely.

So what is left to profit from? The spread between the two months. You are no longer betting on where RELIANCE goes. You are betting on whether the gap between the July price and the August price widens or narrows.

A calendar spread is long one expiry and short another of the same underlying, so you trade the difference between the two months rather than the direction of the market itself.

Why the spread is the cost of carry

Recall from the basis chapter why a future trades above spot. The premium is the cost of carry, the financing cost of holding the underlying through time. A contract that expires further away carries more days, so it usually sits at a wider premium than the nearer contract.

That is exactly why the two months trade at different prices. With RELIANCE spot near Rs 1,318, the July future might sit near 1322 and the August future, with a full extra month of carry, near 1334. The roughly 12 point gap between them is not random. It is one extra month of carry priced into the further contract. When you put on a calendar spread, the value of your position is that carry, and what you are really taking a view on is whether the market's financing cost and sentiment will make that 12 point gap grow or shrink before you close.

Because the two legs move together with the stock, the position has far lower variance than an outright long or short. A 40 point swing in RELIANCE barely touches a calendar spread, while it would be a Rs 20,000 swing on a single lot of 500 shares held outright. The spread breathes gently in a narrow band set by carry, not by the wild daily moves of the stock. That lower variance is precisely why professional desks like it. They are harvesting a small, well understood quantity instead of gambling on direction.

The value of a calendar spread is essentially the cost of carry between the two expiries. Because both legs move with the stock, the direction cancels out and only the spread between the months drives your profit or loss, which makes it a much lower-variance position than an outright future.

The rollover you already know is a calendar spread

Here is the part that should make something click. You have already met a calendar spread without being told its name. It was the rollover.

When you roll a long RELIANCE position from July to August, you sell the July future to close and buy the August future to reopen. For a single moment, before the July leg settles away, you are simultaneously short July and long August. That is exactly a calendar spread. The only difference is intent. A rollover is a calendar spread executed not to harvest the carry but to carry a directional view forward across an expiry.

And the cost of that rollover, the spread you pay, is the calendar spread itself. In the earlier example you sold July at 1322 and bought August at 1334, paying 12 points to keep your long alive one more month. That 12 points was Rs 6,000 on a lot of 500 shares. Seen through today's lens, the rollover cost simply is the price of the calendar spread between the two months. Roll a long every month and you pay that spread every month. Roll a short and you are on the other side, effectively collecting it.

Rolling one long RELIANCE lot from July to August means selling July near 1322 and buying August near 1334. For an instant you are short July and long August at once, which is a calendar spread. The 12 point gap, worth Rs 6,000 on 500 shares, is the price of that spread and the true cost of carrying your view forward.

This is why professionals watch rollover activity so closely. During the rollover week the whole market is putting on calendar spreads at the same time, and the price at which those spreads trade reveals the market's appetite for carrying its view another month.

Basis trading: locking the carry

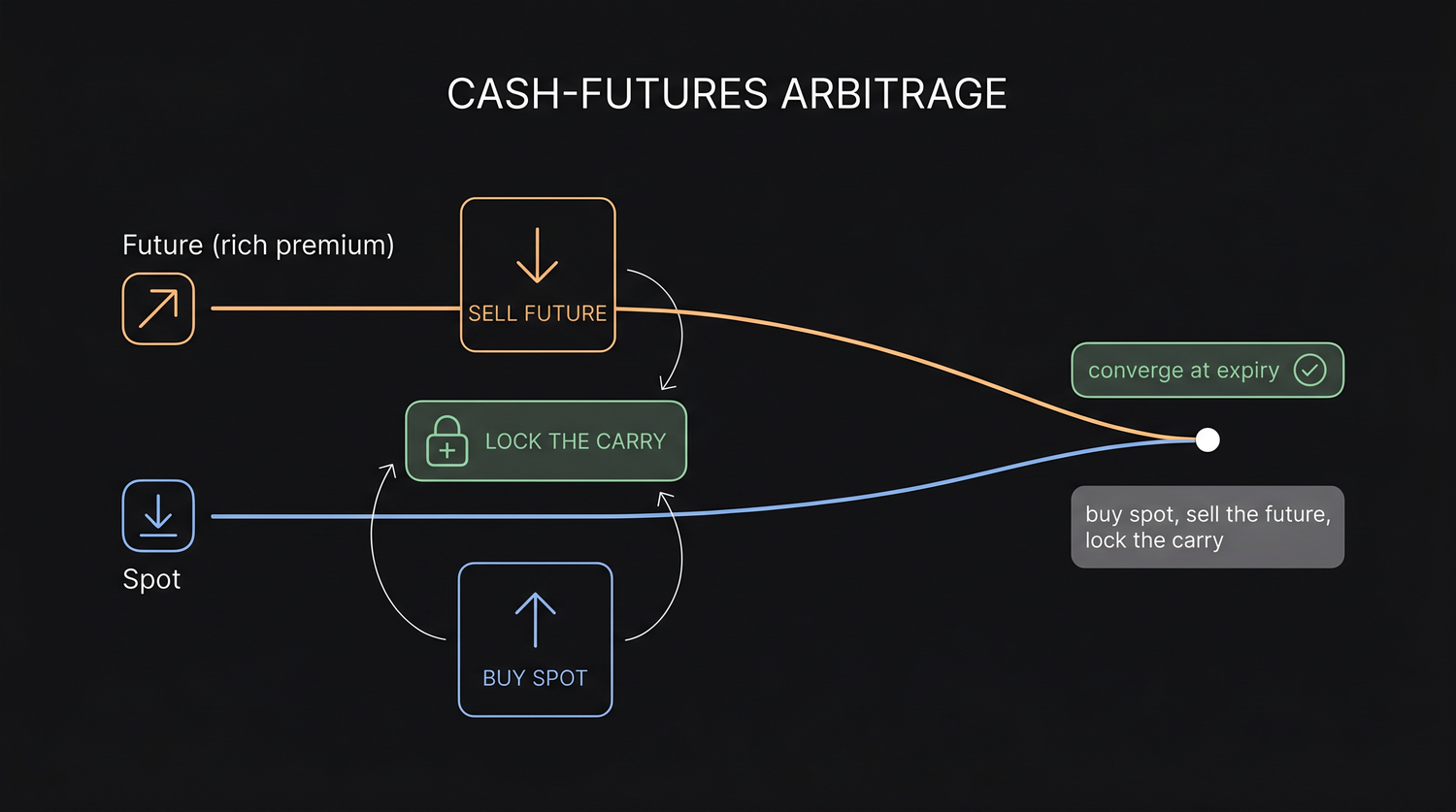

The second professional move explains why the basis behaves at all. It is called basis trading, or cash-futures arbitrage, and it is the mechanism that keeps a future honest.

Imagine the RELIANCE future has run up to a rich premium, far above what the ordinary cost of carry would justify. Say the carry should be worth about 8 points, but eager leveraged buyers have pushed the future to a premium of 20 points over spot. A professional sees free money in that gap. They do two things at the same instant. They buy the actual share in the cash market at Rs 1,318, and they sell the future at the rich 1338. They now own 500 real shares and are short one future against them.

From that moment they are indifferent to where RELIANCE goes. If the stock soars, the shares they hold gain and the short future loses by the same amount. If it crashes, the shares lose and the short future gains. The direction is locked out. What they have captured and locked in is the 20 point premium, the difference between the cheap cash price they paid and the rich futures price they sold.

Now recall convergence from the basis chapter. At expiry the future must settle at the spot price, so the basis must shrink to zero on a known date. That certainty is what makes this trade work. The professional simply holds both legs to expiry. The 20 point premium they sold melts to zero as the contract converges, and that whole gap, minus their real costs, is their profit. They were not predicting the stock. They were harvesting a premium that was guaranteed to disappear.

Because a future must converge to spot at expiry, a premium that is too rich can be locked in for profit by buying the share and selling the future. This arbitrage is the force that pulls an over-stretched future back toward fair value.

Why this keeps the future tethered

The beauty of basis trading is that you do not need to do it for it to protect you. The mere fact that professional desks are ready to pounce on any rich premium means the premium can never get very rich in the first place. The instant a future drifts too far above fair carry, arbitrageurs sell the future and buy the shares, and their selling pushes the future back down toward fair value. The same works in reverse. If a future falls to an unjustified discount, desks buy the cheap future and sell the shares, lifting it back up.

This is the real answer to a question you may have carried since the basis chapter. Why is the future not free to drift wherever traders feel like? Because an army of well capitalised arbitrageurs is standing by to trade any unfair gap back to fair value. The future is tethered to the share by carry, and basis trading is the rope.

You never have to run the arbitrage to benefit from it. The readiness of professional desks to trade away any unfair premium or discount is exactly what keeps a future tracking its underlying within a narrow, carry-defined band.

Why a beginner does not run pure arbitrage

It would be dishonest to send you off thinking this is easy retail money. Pure cash-futures arbitrage is a professional's game for sound reasons.

- It needs scale. The gap between fair carry and the market premium is usually small, often a handful of points, so you must trade large size to earn a worthwhile rupee amount.

- It needs very low costs. Every leg pays brokerage, taxes, and the bid-ask spread, both when buying the shares and when selling the future, and again to unwind. A retail cost stack eats a small mispricing alive.

- It needs full cash for the shares. You are buying 500 actual RELIANCE shares, about Rs 6,59,000, not posting a small margin. There is no leverage helping you, because the whole point is to remove risk, not amplify it.

Put together, those three demands mean the edge belongs to desks with cheap capital, tiny costs, and the size to make a few points worthwhile. A beginner chasing a 4 point premium with retail costs will simply pay it all away in charges. That is the honest verdict, and the same scale and cost demands make pure calendar-spread trading a professional pursuit too.

Do not attempt cash-futures arbitrage as a beginner. The mispricing is small, the costs are real, and you must fund the full value of the shares with no leverage. Understanding the trade is valuable. Trying to run it on a retail account is a quiet way to give your costs to your broker.

So why learn all this if you will not trade it? Because it answers who you are trading against and why prices sit where they do. The premium on your future is set by desks running these calendars and arbitrages. The basis behaves predictably because they enforce it. And a future stays tethered to its share because professionals make money whenever it does not. You now understand the carry not just as a number on your screen but as something living people actively manage. The practical takeaway is humble and useful. Trade direction in the near month, respect the basis as a fair price set by smarter capital, and treat your rollover cost for what it truly is, a calendar spread you are paying to keep your view alive.