The Expiry Calendar and Contract Cycle

At any moment, three monthly contracts trade at once. Learn the near, next and far month, the monthly cycle and expiry day, how to choose which contract to trade, and why a beginner should avoid the thin far-month contract.

- ·Near, next and far month

- ·The monthly contract cycle

- ·Expiry day in the cycle

- ·Choosing which month to trade

- ·Why the far month is thin

- ·Liquidity across the cycle

Open the futures section of any quote screen and look closely at the RELIANCE contracts on offer. You will not see one future. You will see three, each with a different date stamped into its name, each trading at a slightly different price. One of them is busy, with orders flying. The next is quieter. The third barely moves at all. This is not clutter and it is not a choice the exchange made at random. It is a rhythm, a calendar that turns over month after month, and once you understand the beat of it you will never again be surprised by an expiry date or caught holding a contract that is about to vanish.

This chapter is about that rhythm. Not the act of rolling a position, which an earlier chapter covered, but the calendar itself: which contracts exist at any moment, how they are born and how they die, when exactly they expire, and why the last day of a contract behaves differently from every other day. Get the calendar into your bones and the rest of futures trading feels far less mysterious.

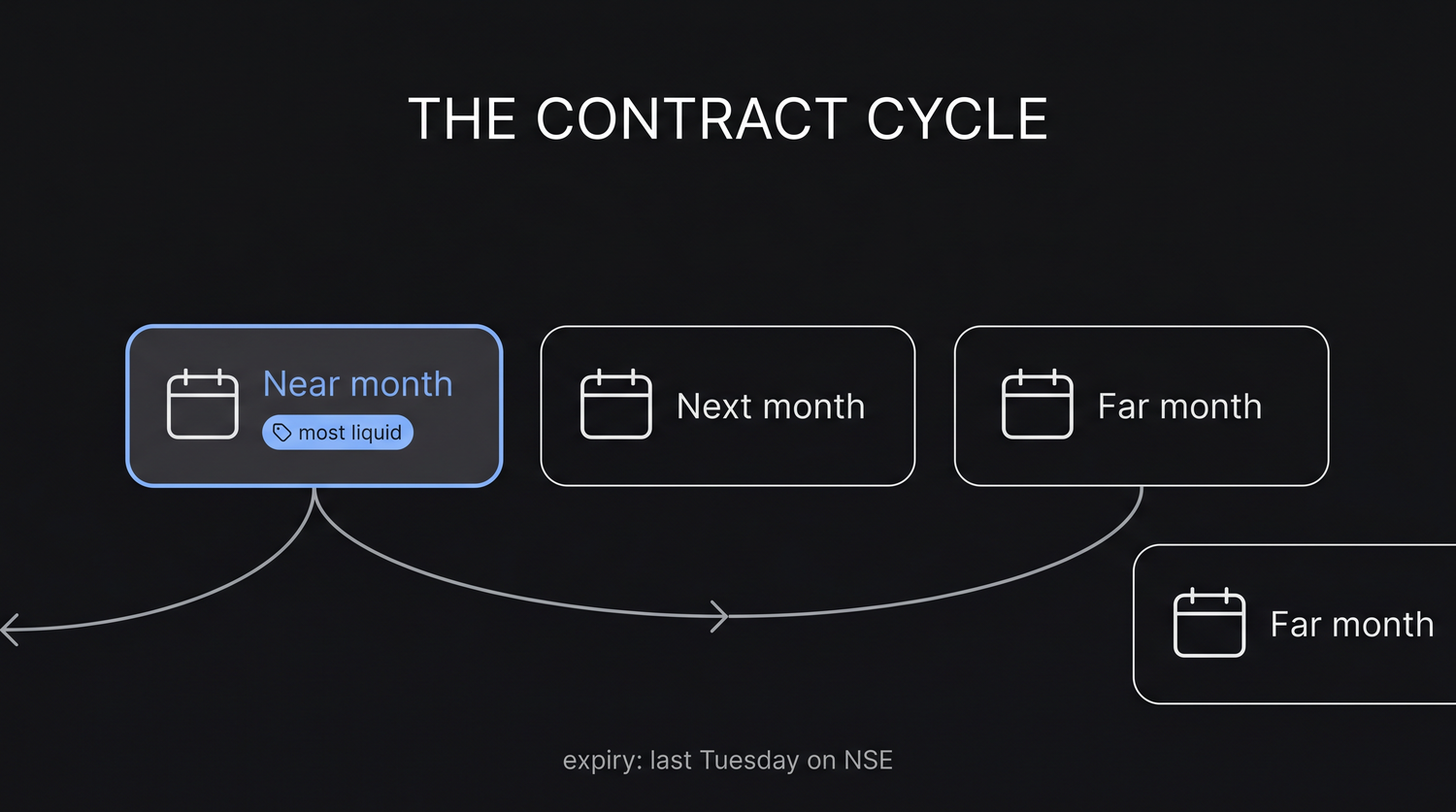

Three contracts trade at once

At any given moment the Indian market lists three monthly futures on a given underlying. They are not three different products. They are the same contract on the same underlying, separated only by when they settle.

- The near month is the contract closest to expiry. For RELIANCE today that is the July future, settling on 28 July 2026. This is where almost all the trading happens. Spreads are tight, volume is heavy, and getting in and out is easy.

- The next month is the one after, the August future. It is reasonably traded but far quieter than the near month, and it comes alive mainly during the rollover window when the crowd starts moving across.

- The far month is the third, the September future. It is genuinely thin. On many days only a handful of contracts change hands, the gap between the buying and selling price is wide, and a single order can shove the price around.

So three doors are always open: July, August, September. Behind each is exactly the same RELIANCE exposure, just delivered on a different date. The price differs a little between them because, as the basis chapter explained, a contract that settles further away carries more days of financing, so it usually sits at a slightly wider premium to the spot.

On any underlying, three monthly futures trade at once: the near month (most liquid), the next month, and the far month (thin). They are the same contract on the same underlying, separated only by their settlement date.

The cycle rolls forward forever

Here is the part that turns a static picture into a living calendar. The three contracts do not stay fixed. They move forward in lockstep, one step every month, and the machinery never stops.

When the near month reaches its expiry and settles, it simply drops off the board. The July future, once 28 July passes, no longer exists. At that point what was the next month becomes the new near month, and what was the far month becomes the new next month. To keep three contracts on offer, the exchange introduces a brand new far month at the back.

So the morning after July expiry, the board reads August, September, October. August is now the busy near month, September has stepped up to be the next month, and October is the freshly listed far month that almost nobody is trading yet. A month later the same thing happens again. September becomes near, October becomes next, November is born at the back. The cycle rolls forward forever, shedding the front contract and growing a new one at the rear, month after month, year after year.

This is why a futures view can be carried indefinitely even though no single contract lasts more than a few months. Think of the three contracts as a conveyor belt. Every month the front one falls off the edge, the others slide forward to fill its place, and a new one is loaded at the back. The belt never empties and it never stops. There is always a fresh contract waiting behind the one expiring, so the instrument is dated but the market in it is perpetual.

The last Tuesday: when the monthly contract expires

A calendar is only useful if you know the exact dates, so commit this rule to memory. On the NSE, where every example in this course trades, the monthly expiry falls on the last Tuesday of the contract month. For the July 2026 cycle that is 28 July 2026, which is indeed the final Tuesday of the month. The August contract will then expire on the last Tuesday of August, September on the last Tuesday of September, and so on down the conveyor belt.

This is the settlement-day rule worth carrying with you everywhere in Indian derivatives:

- NSE derivatives, which includes the NIFTY and BANKNIFTY indices and stock futures such as RELIANCE, settle on Tuesday.

- BSE derivatives, such as the SENSEX, settle on Thursday.

Because every instrument in this course is an NSE instrument, every expiry you meet here lands on a Tuesday. If the scheduled Tuesday happens to be a trading holiday, the expiry simply moves to the previous trading day, but the default to remember is the last Tuesday of the month.

The expiry weekday is set by the exchange, not by the stock. A RELIANCE future and a NIFTY future both settle on a Tuesday because both are NSE products. The same company listed through a BSE derivative would settle on a Thursday instead.

Weekly expiries: short-dated contracts on the index

Monthly contracts are the whole story for stock futures like RELIANCE. But the most active index carries an extra layer on top. The benchmark index future also offers weekly expiries, a fresh short-dated contract that settles every Tuesday rather than only on the last Tuesday of the month.

So alongside the monthly NIFTY future you will find weekly NIFTY contracts that live for just a few days each. In July 2026, NIFTY weeklies would settle on the Tuesdays falling through the month, the 7th, the 14th, the 21st, and finally the 28th, which doubles as the monthly expiry for that cycle. Each weekly contract is born, trades for its handful of days, and settles, while the monthly contract continues underneath.

These short-dated contracts exist because demand exists. Plenty of traders want exposure for only a few days around a known event, and a weekly contract lets them take a tight, short-lived position without committing to a whole month. The trade-off is that weeklies decay and move fast, and the week of their expiry can be jumpy. For a beginner the weekly rhythm is mainly something to be aware of, so that an expiry never sneaks up on you, rather than something to chase.

The benchmark index runs on a weekly heartbeat: a new contract settling every Tuesday. The last Tuesday of the month is special because the weekly expiry and the monthly expiry land on the very same day, which is usually the most active and most volatile session of the cycle.

Expiry day: higher volatility and the final settlement price

Expiry day does not feel like an ordinary trading day, and you should expect that. As a contract nears its final hours, every trader still holding it has to decide: close out, roll forward, or let it settle. All of that activity crowds into the last sessions, positions are unwound in a hurry, and the price can swing more sharply than usual. Higher volatility on expiry day is the norm, not the exception, especially on the last Tuesday when a weekly and a monthly contract expire together.

There is one technical detail about expiry day that genuinely matters, because it decides the number your profit or loss is measured against. Keep two settlement prices apart. On every ordinary trading day your mark-to-market uses the daily settlement price, which the exchange derives from the futures contract itself, normally the volume-weighted average price (VWAP) of the contract over the last 30 minutes of trading. But on expiry the contract is closed out against the final settlement price, and that is taken from the underlying, not from the futures contract. For an index future such as NIFTY it is the closing value of the index on expiry day; for a single-stock future it is the exchange-defined closing price of the underlying share, itself a VWAP of the share over the closing window. The exact methodology is set by the exchange, so confirm it against the current NSE settlement-price circular before you rely on it.

Using a closing-window average of the underlying, rather than one last print, makes the final settlement price robust. No single order can yank it, and the figure that closes out every open contract is a fair reflection of where the market genuinely was as the contract died.

Your profit or loss at expiry is set against the weighted-average closing price, not the last tick you happened to see flash on the screen. Do not assume the final number you glimpsed is the price you settled at. The official settlement value is the averaged figure the exchange publishes for the closing session.

The beginner's rule: live in the near month, know your date

Pull the calendar together and the practical guidance is short and worth following without exception.

First, live in the near month. That is where the liquidity is, where spreads are tight and fills are clean. The next month is for rolling into as expiry approaches, and the thin far month is best left to experienced traders with a specific reason. Trading the busy front contract spares you the hidden cost of dealing where almost nobody else is.

Second, and this is the one that saves beginners real money, always know your expiry date. Every contract you open has a settlement date stamped into its name, and that date is a hard deadline. The whole point of understanding the calendar is so that no position of yours is ever auto-settled by surprise. Mark the last Tuesday on your own calendar the moment you enter. Well before it arrives, decide deliberately whether you will close the position, let it cash-settle, or roll it into the next month. Drifting into an expiry you forgot about is how careless traders get dragged into an outcome they never intended.

You buy one lot of the RELIANCE July future. The name itself tells you the deadline: 28 July 2026, the last Tuesday of the month. On the day you enter, you note that date and plan your exit around it. You are not surprised by expiry, because you read the calendar before you ever pressed buy.

The contract cycle is one of the most reliable structures in all of trading. Three doors are always open, the front one closes each month while a new one opens at the back, and the whole belt advances on the last Tuesday of every month on the NSE. Know which month you are in, know the Tuesday your contract dies, and the calendar becomes a friend that keeps you oriented rather than a trap that catches you out.