Rollover: Moving to the Next Month

Futures expire, but a view can outlast a month. Learn rollover, the act of closing the expiring contract and opening the next one, and what high rollover tells you about market sentiment.

- ·Why contracts expire

- ·Closing and reopening a position

- ·The rollover cost

- ·Rollover percentage as a signal

- ·Expiry-day mechanics

- ·Avoiding the illiquid far month

Every futures contract carries an expiry date stamped into its name. The RELIANCE future for this cycle settles on 28 July 2026, and on that day the contract simply ceases to exist. But a trader's opinion does not politely end on the last Tuesday of the month. You might be convinced RELIANCE is heading higher over the next three months, yet the contract you are holding has only a few weeks of life left. So what happens to your view when the contract dies? You move it forward. That move has a name, and learning to do it cleanly is one of the quiet skills that separates a prepared trader from a flustered one.

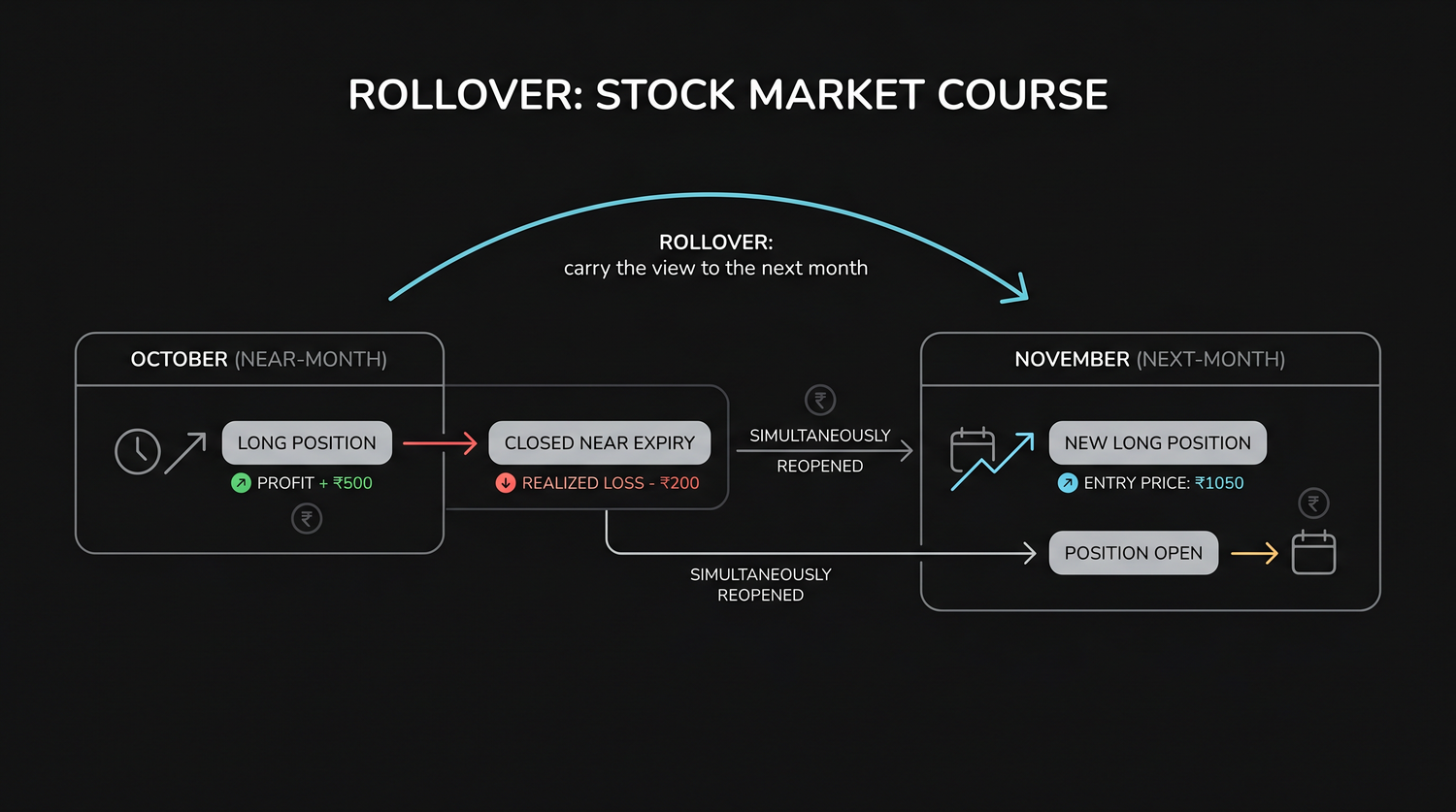

The move is called a rollover, and it is nothing more than carrying an open position from the expiring month into the next month so your market view can outlive a single contract. Almost every position trader who holds futures for more than a few weeks ends up rolling, so it pays to understand exactly what you are doing, what it costs, and what the crowd's rolling behaviour is quietly telling you.

Contracts expire, but views do not

A future is a dated promise. The Indian market always lists several months at once. Right now you can trade the July contract, the August contract, and usually a September contract as well. The near month is the one closest to expiry, July in our example, and it is where almost all the trading happens. The next month is August, and the far month is September.

When July expiry arrives on 28 July 2026, every open July position must be settled. If you still believe in your trade, you do not want to be flat the next morning with no position at all. You want the same exposure in the August contract instead. Rolling over is how you keep your seat at the table when the music for one contract stops.

A rollover means closing your position in the expiring contract and opening the same position in the next month. Your market view survives the expiry of any single contract.

What a rollover actually involves

Rolling is two trades done close together, ideally at the same moment. Suppose you are long one lot of the RELIANCE July future, which is 500 shares. To roll to August you do two things:

- You sell your July long to close it before expiry.

- You buy one lot of the August future to reopen the same long exposure.

After those two trades you own no July future and one lot of August. Your direction is unchanged, your size is unchanged, only the expiry month has moved forward. If you were short instead, you would buy back the July short and sell the August future, the same idea in mirror image.

Most trading platforms let you place both legs almost together so you are not exposed to a wild price swing in the gap between them. The cleaner you do it, the less you pay in slippage and the less you sweat.

The rollover cost: the spread you pay

Rolling is not free. The July and August contracts trade at slightly different prices, and that difference is the rollover cost, sometimes called the roll spread. Remember from the chapter on basis that a future usually trades at a premium to spot because of the cost of carry, and a contract expiring further away carries more days, so it usually sits at a wider premium.

Picture realistic numbers. RELIANCE spot is about Rs 1,318. The July future, close to expiry, might trade near 1322. The August future, with a full extra month of carry, might trade near 1334. To roll a long you sell July at 1322 and buy August at 1334. That 12 point gap is your rollover cost. On one lot of 500 shares that is 12 times 500, which is Rs 6,000 paid to carry the same long position one month further.

That cost is not a penalty or a fee, it is the price of an extra month of carry, the same financing logic you met with the basis. But it is real money, so a trader who rolls a long every month is steadily paying the premium each time. A trader rolling a short is on the other side and effectively collects that spread. Either way, you must factor the roll spread into what you expect the position to earn.

You are long one RELIANCE July lot. To roll, you sell July at 1322 and buy August at 1334. The 12 point spread costs 12 times 500, or Rs 6,000, to carry the same long exposure into the next month. That is the cost of keeping your view alive past 28 July 2026.

The roll spread is easy to ignore because it never shows up as a separate charge. It hides inside the two prices. Always compare the price you exit the near month against the price you enter the next month, and treat the gap as a real cost of holding your view longer.

Rollover percentage as a sentiment signal

Here is where rollovers become interesting beyond the mechanics. In the days leading up to expiry, the whole market is rolling at once, and the exchange data lets you watch how much of the open interest is being carried forward rather than simply closed. This is usually expressed as a rollover percentage: roughly the share of the expiring contract's positions that move into the next month instead of being squared off and abandoned.

You do not need to compute it yourself, but you should know how to read it.

- A high rollover percentage means most traders are carrying their positions forward. They are not done with their view, they want another month. High rolls are usually read as conviction, a sign the prevailing trend has believers willing to pay the carry to stay in.

- A low rollover percentage means many positions are simply being closed and not renewed. Traders are stepping aside rather than committing to another month, which can hint at hesitation or a trend losing support.

Analysts also watch the roll spread alongside the percentage. A high rollover at a rich premium suggests eager, confident longs. Heavy rolling on the short side, or rolls happening at a discount, points the other way. None of this is a crystal ball, and the signal is noisy, but rollover data is one more honest window into what the broader crowd is actually doing with real money rather than what commentators are saying.

Rollover percentage measures how much of an expiring contract's open interest is carried into the next month. High rollovers suggest traders have conviction in the existing trend; low rollovers suggest they are stepping aside. Read it as a hint, never as a certainty.

Expiry-day mechanics

If you never roll and simply hold a contract into its final session, you must understand what happens. For Indian stock futures like RELIANCE, contracts are settled by physical delivery if you carry them to the close of expiry. That means if you are still long one lot at the final bell, you can be obliged to take delivery of 500 actual RELIANCE shares and pay the full value, around Rs 6,59,000, not the small margin you posted. This catches careless beginners badly.

For index futures such as NIFTY and BANKNIFTY, there is no physical share to deliver, so they are cash-settled. Your position simply closes at the final settlement price and the profit or loss is adjusted in cash. No delivery, no surprise share purchase.

The practical lesson is the same for both. Decide before expiry week whether you are closing the position, letting it cash-settle, or rolling it forward. Do not drift into the final hour of a stock future with an open position you never meant to take delivery on. Either square it off or roll it in good time.

For a stock future, treat the expiry date as a hard deadline. Well before 28 July 2026, decide to close the position or roll it to August. Holding a stock future into final settlement can land you with a physical delivery obligation worth lakhs, far beyond the margin you posted.

Why beginners should stay in the near month

You may wonder why not simply trade the August or September contract directly and skip the rolling. The answer is liquidity. Nearly all the volume sits in the near month. The far month often trades thinly, with a wide gap between the buying price and the selling price. That wide spread means you pay more to get in and more to get out, and a large order can move the price against you.

- The near month is the most liquid, with the tightest spreads and the easiest entries and exits.

- The next month becomes liquid mainly during the rollover week as the crowd moves across.

- The far month is usually thin and is best left to experienced traders with a specific reason.

For a beginner the guidance is simple. Trade the near month, where the market is deep and fair, and when expiry approaches, roll your position to the next month during the rollover window when liquidity has shifted there. That keeps you in liquid contracts at every stage and spares you the hidden cost of trading where almost nobody else is.

The takeaway is that expiry is not the end of a trade, only the end of a contract. A rollover lets a genuine view ride from month to month. Do it cleanly, count the spread you pay as a real cost, read the crowd's rollover behaviour as a soft sentiment signal, and never let a stock future drift unattended into its final settlement.