HFT, Colocation & Latency

The microstructure of speed - colocation at NSE, tick-by-tick data, latency arbitrage, and what's feasible for whom.

- ·What HFT actually does

- ·Colocation at NSE/BSE

- ·Tick-by-tick data

- ·Latency arbitrage

- ·The speed arms race

- ·Where retail quants can and can't play

In the time it takes you to blink, a high-frequency trading firm has placed, modified and cancelled thousands of orders. HFT is the part of the market that feels like science fiction - and the part most likely to make a new quant feel hopeless, as if the game is rigged by people with faster computers. The truth is more useful than that fear. By the end of this chapter you'll understand exactly what speed buys, why you can't win that race - and why you don't have to. This is the last piece of microstructure, and it's strangely liberating.

What HFT actually does

Strip away the mystique and HFT is just three familiar activities done very fast and fully automated:

- Market making - quoting both bid and ask on thousands of instruments, earning the spread, managing inventory in microseconds (the professional version of Module B's liquidity provision).

- Latency arbitrage - spotting that the same instrument is momentarily cheaper on one venue than another and trading the gap before it closes.

- Statistical arbitrage at speed - the pairs and index-arb ideas of Module G, but acting on fleeting micro-dislocations that vanish in milliseconds.

None of it is magic or fortune-telling. It's the same logic you're learning, executed faster than a human can perceive - which is exactly why it lives in a world you can't enter on speed alone.

The speed spectrum

Every participant sits somewhere on a spectrum of speed, and the distances are staggering:

The gap between HFT and you isn't a little - it's a factor of tens of thousands. And it isn't a fair fight you could win with a better laptop, because at this level the limit is physics: the speed of light through a cable, the length of the wire to the matching engine. Let's prove your place on that line with real data.

Measure your own latency

Don't take it on faith - time your own round trip to the market:

# How fast is YOUR setup? Time a round trip to the market and compare to HFT.

import os

import statistics

import time

from openalgo import api

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

latencies = []

for _ in range(20):

t0 = time.perf_counter()

client.quotes(symbol="RELIANCE", exchange="NSE") # one round trip to the market

latencies.append((time.perf_counter() - t0) * 1000) # in milliseconds

time.sleep(0.6) # space calls out so rate limits don't skew the timing

latencies.sort()

p95 = latencies[int(len(latencies) * 0.95) - 1]

print(f"Round trips : {len(latencies)}")

print(f"Fastest : {min(latencies):.1f} ms")

print(f"Median : {statistics.median(latencies):.1f} ms")

print(f"95th pct : {p95:.1f} ms")

print(f"Slowest : {max(latencies):.1f} ms")

print("\nAn HFT firm colocated at the exchange measures this in MICROSECONDS - thousands of times faster.")Round trips : 20 Fastest : 32.2 ms Median : 500.1 ms 95th pct : 2191.6 ms Slowest : 2247.8 ms An HFT firm colocated at the exchange measures this in MICROSECONDS - thousands of times faster.

Your fastest call might be a few tens of milliseconds, but typical round trips run into the hundreds - and notice the slow ones, where the broker's rate limits deliberately throttle you. That's a second wall: a retail API won't even let you poll quickly, by design. Whatever your number, compare it to an HFT engine's microseconds. You're not a little behind; you're in a different universe of time.

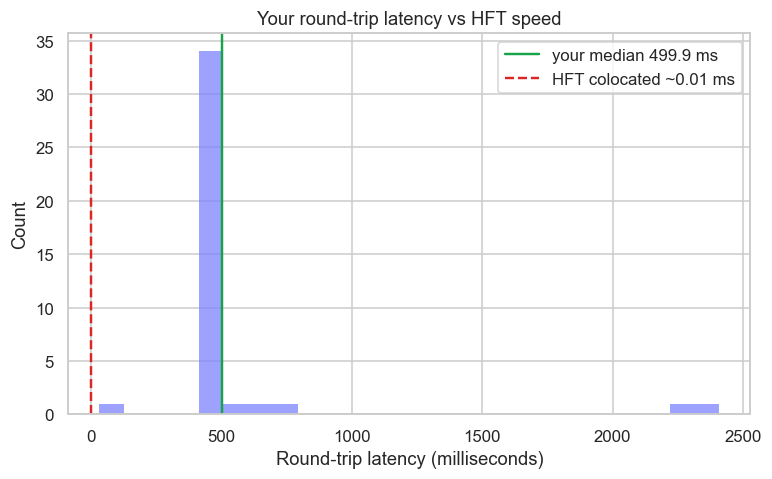

The shape of your latency

Plot every sample and your latency has a distinct, lumpy shape - a fast cluster, then a long tail where throttling and the network bite:

# Your latency has a shape - plot it, and see how far it is from HFT speed.

import os

import time

from pathlib import Path

import matplotlib

matplotlib.use("Agg")

import matplotlib.pyplot as plt

import seaborn as sns

from openalgo import api

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

latencies = []

for _ in range(40):

t0 = time.perf_counter()

client.quotes(symbol="RELIANCE", exchange="NSE")

latencies.append((time.perf_counter() - t0) * 1000)

time.sleep(0.6) # space calls out so rate limits don't skew the timing

sns.set_theme(style="whitegrid")

fig, ax = plt.subplots(figsize=(8, 4.5))

sns.histplot(latencies, bins=25, color="#7c83ff", edgecolor="none", ax=ax)

med = sorted(latencies)[len(latencies) // 2]

ax.axvline(med, color="#16a34a", lw=1.6, label=f"your median {med:.1f} ms")

ax.axvline(0.01, color="#dc2626", lw=1.6, ls="--", label="HFT colocated ~0.01 ms")

ax.set_title("Your round-trip latency vs HFT speed")

ax.set_xlabel("Round-trip latency (milliseconds)")

ax.set_ylabel("Count")

ax.legend()

out = Path(__file__).with_suffix(".png")

plt.savefig(out, dpi=110, bbox_inches="tight")

print(f"Median {med:.1f} ms - roughly {med / 0.01:,.0f}x slower than a colocated HFT engine. Saved {out.name}")Median 499.9 ms - roughly 49,988x slower than a colocated HFT engine. Saved 02_latency_chart.png

The red line marks HFT's colocated speed - so far to the left of your distribution it's practically at zero. No amount of code optimisation on your side moves your cloud of dots anywhere near it. The race is over before it starts.

Colocation and the arms race

How do HFT firms get to microseconds? Colocation - they rent rack space for their servers inside the exchange's own data centre, a few metres of cable from the matching engine. NSE and BSE both offer it. From there, the competition becomes absurd and literal: shaving nanoseconds by shortening cables, using faster network cards, even choosing a rack closer to the engine. They consume tick-by-tick data feeds (every single order and trade, not the throttled snapshots you get) and react in hardware. It's a genuine arms race, and the price of entry is crores.

This is why latency-sensitive strategies are off-limits to retail. Any edge that depends on being first - sub-second arbitrage, sniping a stale quote, reacting to a print before others - belongs to the colocated firms. If your strategy's profit comes from speed, you will lose. Build nothing that races them.

Where a retail quant can - and can't - play

Here's the liberating part. Speed is just one axis of competition, and HFT dominates only that one. You compete on the axes they ignore:

- Time horizon. HFT lives in microseconds and holds for milliseconds. Hold for days or weeks and their speed advantage is completely irrelevant - a swing or positional edge doesn't care who was 10 microseconds faster.

- Research depth. A better signal - a real, well-validated edge (Modules C-G) - beats a faster connection when the holding period is long.

- Niches and capacity. HFT needs liquid, high-volume instruments to deploy capital at speed. Smaller, slower, less crowded corners of the market are often beneath their notice - and open to you.

You will never win on speed, so don't try. Win on horizon, research and patience - edges that take minutes, hours or days to play out, where being thoughtful beats being fast. Almost everything in the rest of this course is built for exactly that game.

Try it yourself

- Run the latency example at a quiet time and a busy market hour. Does your median round trip get slower when the market is active?

- Look up the cost of an NSE colocation rack and a tick-by-tick data feed. Roughly how large would a strategy have to be to justify that fixed cost?

- List your own strategy ideas and mark each "speed-sensitive" or "horizon-based". The horizon-based ones are the ones worth your time.

Recap

- HFT is ordinary market-making, arbitrage and stat-arb done in microseconds, fully automated - fast, not magic.

- The speed spectrum runs from HFT (microseconds) through prop desks (~1 ms) to retail algos (hundreds of ms) and humans (seconds) - a gap of tens of thousands of times, limited by physics.

- Measuring your own round trip proves it: you're in the hundreds of milliseconds, and broker rate limits stop you polling fast anyway.

- Colocation (servers inside the exchange) and tick-by-tick feeds power the arms race - and put all latency-sensitive strategies out of retail reach.

- You compete not on speed but on time horizon, research depth and overlooked niches - which is exactly what the rest of this course builds.

That completes Module B - market microstructure, from the order book to the speed of light. We now leave the plumbing behind and pick up the quant's other essential toolkit: the mathematics of markets. Next, we confront what returns actually look like, and why their fat-tailed reality breaks the neat assumptions of classical finance.