Trading Volatility

Volatility as an asset - variance trades, gamma scalping, the vol risk premium, and Indian expiry-day effects.

- ·Volatility as an asset

- ·The volatility risk premium

- ·Gamma scalping

- ·Variance & straddle P&L

- ·Expiry-day effects

- ·Selling vs buying vol

Here is the idea that separates an options trader from someone who merely buys calls and puts: you can trade volatility itself, with no view on direction at all. You can bet the market will move a lot, or barely move, and profit from being right about the size of the swing regardless of which way it goes. Given what we learned in Chapter 11 - that volatility, unlike direction, is genuinely forecastable - this is the most natural quant trade in the options world. It's also where India's enormous options market truly lives. Let's finish the derivatives module by trading vol.

Volatility as an asset

When you buy an at-the-money call and an at-the-money put together - a straddle - you don't care which way the market goes; you only care that it moves enough. You've bought volatility. Sell that same pair and you've sold volatility - you now want the market to sit still. Volatility has become the thing you're trading, an asset in its own right, completely separate from direction.

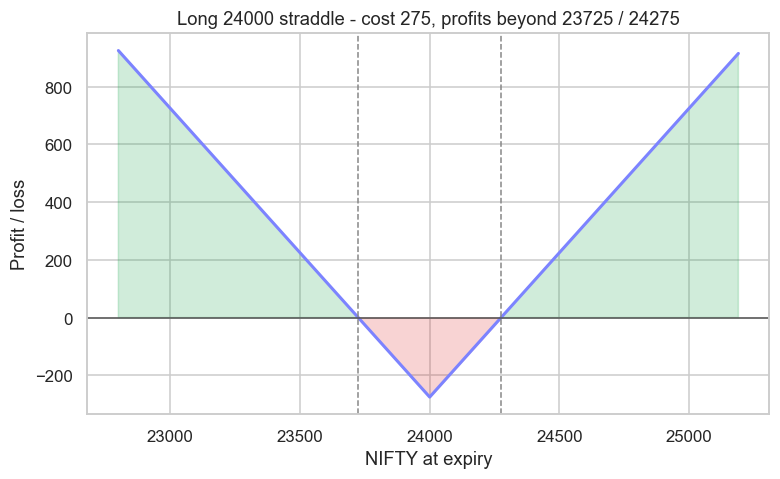

The long straddle: buying a big move

Let's price and plot a real one - a long Nifty straddle, buying both the ATM call and put:

# A long straddle buys volatility: it profits from a BIG move either way.

import os

from pathlib import Path

import matplotlib

matplotlib.use("Agg")

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

from openalgo import api

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

STRIKE = 24000

call = client.quotes(symbol=f"NIFTY30JUN26{STRIKE}CE", exchange="NFO")["data"]["ltp"]

put = client.quotes(symbol=f"NIFTY30JUN26{STRIKE}PE", exchange="NFO")["data"]["ltp"]

cost = call + put # premium paid for the straddle

spots = np.arange(STRIKE - 1200, STRIKE + 1200, 10)

payoff = np.abs(spots - STRIKE) - cost # long straddle P&L at expiry

lower, upper = STRIKE - cost, STRIKE + cost # breakevens

sns.set_theme(style="whitegrid")

fig, ax = plt.subplots(figsize=(8, 4.5))

ax.plot(spots, payoff, color="#7c83ff", lw=2)

ax.axhline(0, color="#555", lw=1)

ax.fill_between(spots, payoff, 0, where=payoff > 0, color="#16a34a", alpha=0.2)

ax.fill_between(spots, payoff, 0, where=payoff < 0, color="#dc2626", alpha=0.2)

ax.axvline(lower, color="#888", ls="--", lw=1)

ax.axvline(upper, color="#888", ls="--", lw=1)

ax.set_title(f"Long {STRIKE} straddle - cost {cost:.0f}, profits beyond {lower:.0f} / {upper:.0f}")

ax.set_xlabel("NIFTY at expiry")

ax.set_ylabel("Profit / loss")

out = Path(__file__).with_suffix(".png")

plt.savefig(out, dpi=110, bbox_inches="tight")

print(f"Straddle cost {cost:.0f} (call {call} + put {put}). Breaks even at {lower:.0f} and {upper:.0f}. Saved {out.name}")Straddle cost 275 (call 166.75 + put 108.45). Breaks even at 23725 and 24275. Saved 02_straddle.png

The payoff is a clean V. You paid 275 points (call + put) for the privilege, so you lose if Nifty expires near the strike - the worst case is a quiet market that wastes your premium. But break out beyond the breakevens (23725 or 24275) in either direction and you profit, more the further it runs. A long straddle is a pure bet that the coming move will be bigger than the market has priced in. Which raises the obvious question: what has the market priced in?

The volatility risk premium

This is the deepest fact in options trading. On average, implied volatility exceeds the volatility that actually shows up. Compare them directly:

# The volatility risk premium: implied vol usually exceeds what actually happens.

import os

from datetime import datetime, timedelta

from openalgo import api

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

# Implied: what options price in (India VIX, ~30-day forward-looking).

vix = client.quotes(symbol="INDIAVIX", exchange="NSE_INDEX")["data"]["ltp"]

# Realized: what the market actually did over the last 30 sessions.

end = datetime.now().strftime("%Y-%m-%d")

start = (datetime.now() - timedelta(days=90)).strftime("%Y-%m-%d")

r = client.history(symbol="NIFTY", exchange="NSE_INDEX", interval="D",

start_date=start, end_date=end)["close"].pct_change().dropna()

realized = r.tail(30).std() * (252 ** 0.5) * 100

print(f"Implied volatility (India VIX) : {vix:.2f}%")

print(f"Realized volatility (last 30d) : {realized:.2f}%")

print(f"Volatility risk premium : {vix - realized:+.2f}%")

print("\nImplied usually exceeds realized - the premium that option SELLERS harvest for bearing risk.")

print("Like insurance: buyers overpay for protection on average, sellers collect it - until a crash.")Implied volatility (India VIX) : 13.39% Realized volatility (last 30d) : 11.76% Volatility risk premium : +1.63% Implied usually exceeds realized - the premium that option SELLERS harvest for bearing risk. Like insurance: buyers overpay for protection on average, sellers collect it - until a crash.

India VIX implies 13.4%, but the market actually delivered under 12% - a volatility risk premium of about +1.6%. This gap is persistent and structural: option buyers are buying insurance and willingly overpay for protection, while option sellers collect that premium for bearing the risk - exactly like an insurance company. Selling volatility harvests this premium, and it's one of the most reliable income strategies in markets... with a terrifying catch we'll come to.

Buy versus sell volatility

The two sides of the vol trade are mirror images, and you must know which you're on:

The buyer has positive gamma (gains as the market moves, either way) but bleeds theta every day. The seller is the reverse: pocketing theta daily but exposed to negative gamma - small steady gains, then a sudden brutal loss if the market lurches. The volatility risk premium is the seller's reward for standing on that trapdoor.

Gamma scalping

There's a purer way to trade the implied-versus-realized gap: gamma scalping. Hold a long-gamma position (like the straddle) and continuously delta-hedge it - buying the underlying when it dips, selling when it rises. Each hedge locks in a small profit from the market's wiggles. If the volatility you actually capture (realized) exceeds what you paid (implied), you win; if not, theta grinds you down. It's the cleanest expression of "I think realized vol will beat implied," and it's a staple of professional options desks.

Expiry-day games

India puts its own stamp on all of this through weekly expiries. On expiry day, time decay is savage - an option's entire remaining value evaporates in hours - so enormous flows of premium-selling concentrate there, and the underlying can get "pinned" near a heavily-traded strike. The risk-reward warps: sellers harvest fat theta, but a sudden move can inflict outsized losses in minutes. A huge share of India's record options volume is this weekly expiry-day vol-selling - and a whole family of quant strategies (Module G) is built around its rhythm.

Selling volatility is famously "picking up pennies in front of a steamroller." The income is steady and the win rate is high - which is exactly what makes it dangerous, because it lulls you into sizing up right before the rare day the steamroller arrives. Many blow-ups in history were naked vol sellers. If you sell vol, defined risk and hard position limits aren't optional - they're the whole strategy.

Try it yourself

- Build a short straddle payoff (flip the sign). Confirm it's an inverted V - steady profit if Nifty sits near the strike, escalating loss if it runs.

- Track the vol risk premium daily for a week. Is implied consistently above realized, and does the gap shrink when the market gets turbulent?

- Compare a weekly-expiry straddle's cost to a monthly one. How much cheaper is the weekly - and how much less room does it give the market to move?

Recap

- You can trade volatility itself - a straddle buys or sells a big move with no directional view.

- A long straddle profits if the market moves beyond its breakevens; its worst case is a calm market that wastes the premium.

- The volatility risk premium - implied vol usually exceeds realized (+1.6% here) - is the structural edge that option sellers harvest, like insurers.

- Long vol is positive-gamma/negative-theta (wants storms); short vol is the reverse (wants calm, collects premium, carries tail risk); gamma scalping trades the implied-vs-realized gap directly.

- India's weekly expiries concentrate vicious theta decay and pin risk into expiry day - huge volume, huge opportunity, and the ever-present steamroller that makes risk limits non-negotiable.

That completes Module E - we've priced options with Black-76, read the volatility surface, and traded vol itself. Now we zoom out from the single trade to the whole portfolio: how to combine many positions so that diversification, sizing and risk control turn a collection of edges into a survivable book.