Limit Order Book Fundamentals

Bids, asks and depth - the live queue where every Indian trade is matched, read straight from real depth data.

- ·Bids, asks and depth

- ·Market vs limit orders

- ·Reading the depth ladder

- ·Total buy vs sell quantity

- ·Disclosed and iceberg quantity

- ·Reading depth() data

Until now we've talked about "the price" as if it were a single number. It isn't. The last traded price is just the most recent handshake; the next price is decided by a hidden queue of orders waiting to trade - the limit order book. This is the beating heart of every market, the place where liquidity lives and where every quant edge is ultimately born or lost. If Module C teaches you one thing, let it be how to read this book. Let's open it.

What's really behind a price

The book has two sides: bids (resting buy orders, stacked below the price) and asks (resting sell orders, stacked above). Each line is a promise: "I'll buy 14 lots at 6819," "I'll sell 11 at 6822." Here's a live one - on an MCX crude contract, because commodities trade into the night while NSE and BSE are shut:

# The order book: the live queue of who wants to buy and sell, and at what price.

import os

from openalgo import api

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

# MCX commodities trade into the night, so the book is live even after NSE/BSE close.

SYMBOL, EXCHANGE = "CRUDEOIL20JUL26FUT", "MCX"

d = client.depth(symbol=SYMBOL, exchange=EXCHANGE)["data"]

print(f"{SYMBOL} LTP {d['ltp']}\n")

print(f"{'BID qty':>9s}{'BID':>10s} | {'ASK':<10s}{'ASK qty':<9s}")

for bid, ask in zip(d["bids"], d["asks"]):

print(f"{bid['quantity']:>9d}{bid['price']:>10.1f} | {ask['price']:<10.1f}{ask['quantity']:<9d}")

best_bid, best_ask = d["bids"][0]["price"], d["asks"][0]["price"]

print(f"\nBest bid {best_bid} | Best ask {best_ask} | Spread {best_ask - best_bid:.1f}")

print(f"Resting buy qty {d['totalbuyqty']} vs sell qty {d['totalsellqty']} - a rough read on pressure")CRUDEOIL20JUL26FUT LTP 6820.0

BID qty BID | ASK ASK qty

2 6820.0 | 6822.0 11

14 6819.0 | 6823.0 11

21 6818.0 | 6824.0 15

12 6817.0 | 6825.0 14

22 6816.0 | 6826.0 37

Best bid 6820.0 | Best ask 6822.0 | Spread 2.0

Resting buy qty 71 vs sell qty 88 - a rough read on pressureRead it like a staircase meeting in the middle. The highest someone is willing to pay (best bid) sits just below the lowest someone is willing to sell at (best ask). Nothing trades in the gap between them; a trade only happens when someone agrees to cross it. Everything a quant cares about - liquidity, cost, short-term pressure - is visible right here, in a snapshot most traders never look at.

Price first, then time

How does the exchange decide whose order fills when a buyer finally arrives? Two simple rules, applied in order - price-time priority:

Price priority: the best price always goes first - a sell hits the highest bid (6820) before touching 6819. Time priority: among orders at the same price, the one that arrived earliest fills first - a strict first-in, first-out queue. That's the whole matching engine. It sounds trivial, but it's why being early at a price matters, why HFT firms fight over microseconds (Module C, later), and why a large order eats through several levels and moves the price.

Market orders vs limit orders

You interact with this book in two fundamentally different ways:

- A limit order joins the queue at a price you choose. You might get a great price - or never fill at all if the market walks away. You're a liquidity provider.

- A market order crosses the spread to trade immediately against the best resting orders. You're guaranteed a fill, but you pay for the privilege by giving up the spread. You're a liquidity taker.

Every order is a trade-off between certainty and price. Market orders buy certainty and pay the spread; limit orders chase a better price and risk not trading at all. A quant chooses deliberately - and Module G's execution chapter is entirely about choosing well on large orders.

The spread is a real cost

Look back at the live book: best bid 6820, best ask 6822 - a spread of 2. If you buy at market you pay 6822; if you immediately sell at market you receive 6820. That difference vanishes the instant you trade - it's a cost you pay before the price has moved at all. Liquid contracts have razor-thin spreads; illiquid ones can quietly cost you far more than brokerage and STT combined. We'll formalise spread, depth and impact as the true price of liquidity in the next chapter.

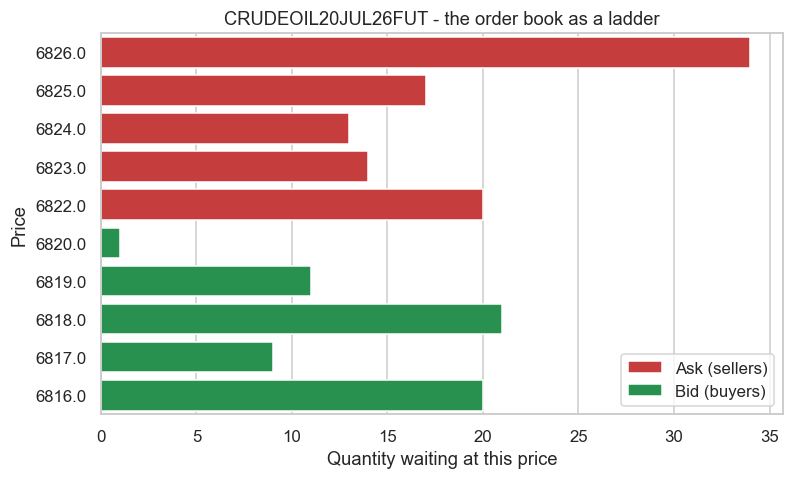

Picture the book

Numbers in a table are hard to feel. Plot the same order book as a ladder and the shape of supply and demand jumps out:

# Picture the order book: resting buy demand (green) vs sell supply (red) by price.

import os

from pathlib import Path

import matplotlib

matplotlib.use("Agg")

import matplotlib.pyplot as plt

import pandas as pd

import seaborn as sns

from openalgo import api

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

SYMBOL, EXCHANGE = "CRUDEOIL20JUL26FUT", "MCX"

d = client.depth(symbol=SYMBOL, exchange=EXCHANGE)["data"]

bids = pd.DataFrame(d["bids"]).assign(side="Bid (buyers)")

asks = pd.DataFrame(d["asks"]).assign(side="Ask (sellers)")

book = pd.concat([asks, bids]).sort_values("price", ascending=False)

book["level"] = book["price"].map(lambda p: f"{p:.1f}")

sns.set_theme(style="whitegrid")

fig, ax = plt.subplots(figsize=(8, 4.5))

sns.barplot(data=book, x="quantity", y="level", hue="side", dodge=False,

order=book["level"], palette={"Bid (buyers)": "#16a34a", "Ask (sellers)": "#dc2626"}, ax=ax)

ax.set_title(f"{SYMBOL} - the order book as a ladder")

ax.set_xlabel("Quantity waiting at this price")

ax.set_ylabel("Price")

ax.legend(title="")

out = Path(__file__).with_suffix(".png")

plt.savefig(out, dpi=110, bbox_inches="tight")

print(f"Best bid {d['bids'][0]['price']} best ask {d['asks'][0]['price']}. Saved {out.name}")Best bid 6820.0 best ask 6822.0. Saved 02_depth_ladder.png

Green bars are resting buyers, red bars resting sellers, stacked by price. Comparing the total green against the total red - the order-book imbalance - gives a rough read on near-term pressure: far more resting buyers than sellers can hint at support beneath the price. Treat it as one weak clue among many, never a standalone signal - it can flip in a second, and large players deliberately hide their true size.

A note on Indian order types

The book is richer than just market and limit. On Indian exchanges you'll also meet IOC (immediate-or-cancel - fill what you can now, kill the rest), SL / SL-M (stop-loss orders that wake up only when a trigger price is hit), GTT (good-till-triggered, resting for days), and disclosed / iceberg quantity (showing only part of a big order so you don't reveal your full hand). Each is a different way of interacting with price-time priority - and a quant picks the type that leaks the least information.

Try it yourself

- Point the order-book example at

GOLDM03JUL26FUT(MCX). Is gold's spread tighter or wider than crude's, relative to its price? - During market hours, switch to an NSE stock like

SBIN(exchangeNSE) and watch the book fill with real bids and asks. - Compute the order-book imbalance as

totalbuyqty / (totalbuyqty + totalsellqty). Track it over a few minutes - does it predict the next tick, or is it noise?

Recap

- "The price" is just the last handshake; the limit order book - resting bids below and asks above - decides the next one.

- Exchanges match on price-time priority: best price first, then earliest order at that price (FIFO).

- Limit orders join the queue (provide liquidity, risk no fill); market orders cross the spread (take liquidity, pay for certainty).

- The bid-ask spread is a genuine, immediate cost; order-book imbalance is a weak pressure clue, not a signal.

- Indian markets add IOC, SL/SL-M, GTT and iceberg order types - each a different way to interact with the book while leaking less information.

The book shows us what's resting at each price. Next we ask the deeper question every execution desk lives on: how much will my own order move the price - the economics of liquidity, spread and market impact.