Algorithmic Trading Foundations

What an algorithmic strategy actually is - the loop from data to signal to order to risk, and the architecture every automated system shares.

- ·The algo trading loop

- ·Signal, sizing and execution layers

- ·Event-driven vs polling

- ·State and idempotency

- ·OpenAlgo as an order gateway

- ·From idea to running bot

A trading idea in your head is worth nothing until it runs without you. The leap from I think a fast moving average crossing a slow one means go long to a process that watches the market, decides, sizes the trade, fires the order, and checks itself - hundreds of times, unattended, without doing something reckless at 2:47 in the afternoon - is the leap this whole module is about. Module D is execution and technology: how a decision actually becomes a fill. We begin at the foundation, the shape that every automated strategy shares no matter how slow or how fast, from a once-a-day rebalance to a microsecond market maker: the algo loop.

The algo loop: data, signal, sizing, order, risk

Strip any trading bot down to its skeleton and you find the same five stages, running in a circle. Market data comes in - a bar, a quote, a depth update. A signal turns that data into an opinion: long, short, or flat. Sizing turns the opinion into a quantity, scaled to your risk budget rather than your conviction. The order carries that quantity to the exchange. And a risk layer sits across the whole thing, clipping size, blocking trades that breach a limit, and able to halt everything. Then the next bar arrives and the loop turns again.

The single most important discipline in bot design is to keep these stages separate. The signal should not know how big your account is. The sizing should not know which broker you use. The risk gate should be the last word, independent of how clever the signal feels. When you braid them together - sizing logic buried inside the signal, risk checks sprinkled through the order code - you get a system nobody can reason about, and reasoning about it is the only thing standing between you and a runaway loss.

Every algorithmic strategy is the same loop: data leads to signal leads to sizing leads to order leads to risk, then back to data. Build the five stages as separate, testable pieces. The signal forms an opinion; sizing scales it to risk; the order executes it; the risk layer can always say no.

Event-driven versus polling

There are two ways to make the loop turn, and the choice colours your whole architecture. Polling means you ask on a timer: every second, every minute, you pull the latest quote or the latest bar and run the loop once. It is simple, easy to reason about, and perfectly adequate for strategies whose edge lives on the scale of minutes or days. Its weakness is latency and waste - you might poll a hundred times and find nothing changed, or miss a sharp move that happened between two polls.

Event-driven means the market pushes to you: a websocket streams every tick or depth change, and each message triggers one turn of the loop. You react the instant something happens, which is the only way to compete where microseconds matter. The cost is complexity - you now handle out-of-order messages, reconnections, buffering, and bursts. Most retail and systematic strategies are happily polling; the higher you climb toward high-frequency work, the more the world becomes event-driven, and Chapter 32 goes deep on the feeds that drive it.

Polling trades latency for simplicity; event-driven trades simplicity for speed. Pick the slowest mechanism your edge can tolerate. A daily-rebalance strategy that switches to a tick feed has added enormous fragility and bought nothing. Match the clock of your infrastructure to the clock of your alpha.

State and idempotency

A naive loop computes a signal and sends an order. A correct loop remembers what it has already done. The bot is a state machine: at any moment it is flat, long, or short, and the only thing that should move it between states is a genuine change in the signal. This is why our first example does not blast an order on every bar where the fast average sits above the slow one - it acts only when the desired state actually flips, and skips the bar otherwise.

That skip is idempotency: applying the same instruction twice must have the same effect as applying it once. Networks retry. Processes crash and restart mid-session. A websocket can deliver the same tick twice. If "go long" naively appends a buy each time it is seen, a restart that replays the morning will leave you triple-long by lunch. The defence is to make every decision relative to current state, not to fire blind. Watch the loop step through ninety recent one-minute bars of RELIANCE:

# The algo loop on real 1m bars: data -> signal -> sizing -> order intent -> risk. No orders sent.

import os

from datetime import datetime, timedelta

import numpy as np

from openalgo import api, ta

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

# --- DATA: recent 1m bars for one liquid name ---

end = datetime.now().strftime("%Y-%m-%d")

start = (datetime.now() - timedelta(days=6)).strftime("%Y-%m-%d")

df = client.history(symbol="RELIANCE", exchange="NSE", interval="1m",

start_date=start, end_date=end)

close = df["close"].values

stamps = df.index

# --- SIGNAL: 9/21 EMA crossover, computed once, vectorised ---

fast = np.asarray(ta.ema(df["close"], 9))

slow = np.asarray(ta.ema(df["close"], 21))

up = ta.crossover(fast, slow) # fast crosses above slow -> go long

dn = ta.crossunder(fast, slow) # fast crosses below slow -> go flat

BUDGET, MAX_QTY = 100_000, 60 # sizing budget and a hard position cap (risk)

position, held, n_signals, blocked = 0, 0, 0, 0

print("time price fast slow signal -> intent qty")

# --- LOOP: walk the most recent bars as if they arrived one by one ---

for i in range(len(close) - 90, len(close)):

if not (up[i] or dn[i]):

continue

target = 1 if up[i] else 0 # desired state from the signal

if target == position: # IDEMPOTENCY: already there, skip

continue

price = close[i]

if target == 1: # SIZING on entry

want = int(BUDGET // price)

qty = min(want, MAX_QTY) # RISK gate: clip to position cap

blocked += qty < want

intent, held = "BUY (enter)", qty

else: # exit flattens whatever we hold

qty, intent, held = held, "SELL (exit)", 0

print(f"{stamps[i]:%H:%M} {price:7.1f} {fast[i]:6.1f} {slow[i]:6.1f} "

f"{'up' if up[i] else 'dn'} -> {intent:11s} {qty:3d}")

position, n_signals = target, n_signals + 1

print(f"\n{n_signals} signals in the last 90 bars; {blocked} risk-capped; final state: "

f"{'LONG' if position else 'FLAT'}. (sandbox-safe, no orders placed)")time price fast slow signal -> intent qty 14:08 1321.8 1321.6 1321.6 up -> BUY (enter) 60 14:13 1319.3 1321.2 1321.4 dn -> SELL (exit) 60 14:37 1319.9 1319.7 1319.7 up -> BUY (enter) 60 14:38 1319.1 1319.6 1319.7 dn -> SELL (exit) 60 14:53 1319.7 1318.5 1318.4 up -> BUY (enter) 60 15:15 1318.3 1319.2 1319.2 dn -> SELL (exit) 60 6 signals in the last 90 bars; 3 risk-capped; final state: FLAT. (sandbox-safe, no orders placed)

Six state changes fired across those ninety bars, three of them sized at the position cap rather than the raw budget quantity, and the bot finished the window flat. Notice the risk gate doing its quiet job: the budget wanted more shares than the cap allowed, so the order was clipped to 60 every time. The signal proposes; risk disposes. And notice the rapid in-and-out - a long at 14:08 reversed five minutes later, another reversed in a single bar. That churn is not a bug in the code; it is the honest behaviour of a raw crossover on noisy intraday data, and it is exactly the kind of cost-bleeding whipsaw a real execution layer has to tame.

The most expensive bug in automated trading is not a bad signal - it is a duplicated or runaway order. A loop that re-sends because a confirmation was slow, or re-fires every bar instead of on a state change, can build a position you never intended. Treat current position as the source of truth, make every order idempotent, and reconcile against the broker's order book before trusting your own memory.

OpenAlgo as the order gateway

The fourth stage - the order - is where your tidy Python meets the messy outside world. You do not want strategy code speaking a different dialect for every broker, juggling auth tokens and symbol formats and rate limits. That job belongs to an order gateway: a single, normalised interface that takes a clean instruction like buy 60 RELIANCE NSE at market and handles the translation, the credentials, and the plumbing to whichever broker sits behind it.

This is the role OpenAlgo plays. Your signal and sizing logic call one consistent Python and REST interface; OpenAlgo carries the order onward and hands back order IDs and fills you can reconcile. It also offers an analyzer mode - sandbox trading - that runs the identical code path and validates every order without sending a single real one to the exchange. The same five-stage loop you just watched can run in sandbox first, prove that its state machine and risk gate behave, and only then be pointed at a live account by flipping a setting, not by rewriting the bot.

Always run a new bot in analyzer (sandbox) mode until its loop, state handling, and risk limits are boringly predictable. Because the code path is identical to live, a clean sandbox run is real evidence - not a separate toy. Promote to live only after the sandbox version has survived a full session without a surprise.

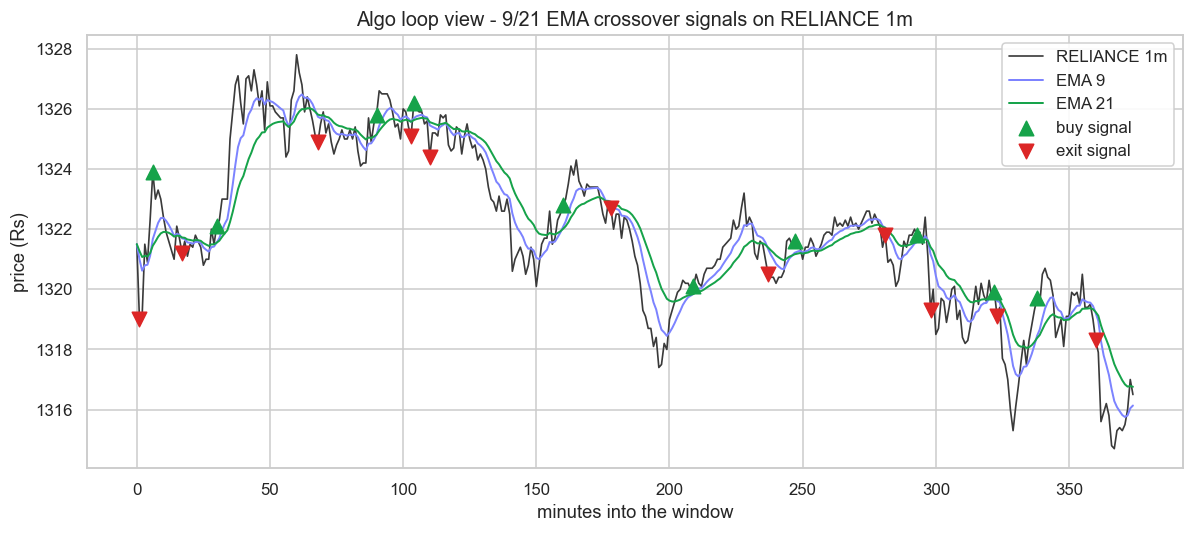

What the bot sees

The print loop shows the decisions; a picture shows the world that produced them. Here is one full session of RELIANCE one-minute bars with the two moving averages and every crossover marked, so you can see precisely what the bot reacted to:

# What the bot sees: a 9/21 EMA crossover firing on a recent RELIANCE intraday series.

import os

from datetime import datetime, timedelta

from pathlib import Path

import matplotlib

matplotlib.use("Agg")

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

from openalgo import api, ta

client = api(

api_key=os.getenv("OPENALGO_API_KEY", "your_api_key_here"),

host=os.getenv("OPENALGO_HOST", "http://127.0.0.1:5000"),

)

end = datetime.now().strftime("%Y-%m-%d")

start = (datetime.now() - timedelta(days=6)).strftime("%Y-%m-%d")

df = client.history(symbol="RELIANCE", exchange="NSE", interval="1m",

start_date=start, end_date=end).tail(375) # ~one session

close = df["close"]

fast, slow = ta.ema(close, 9), ta.ema(close, 21)

up = ta.crossover(fast, slow)

dn = ta.crossunder(fast, slow)

t = np.arange(len(close))

sns.set_theme(style="whitegrid")

fig, ax = plt.subplots(figsize=(11, 5))

ax.plot(t, close.values, color="#3a3a3a", lw=1.1, label="RELIANCE 1m")

ax.plot(t, fast, color="#7c83ff", lw=1.3, label="EMA 9")

ax.plot(t, slow, color="#16a34a", lw=1.3, label="EMA 21")

ax.scatter(t[up], close.values[up], marker="^", s=90, color="#16a34a", zorder=5, label="buy signal")

ax.scatter(t[dn], close.values[dn], marker="v", s=90, color="#dc2626", zorder=5, label="exit signal")

ax.set_title("Algo loop view - 9/21 EMA crossover signals on RELIANCE 1m", fontsize=13)

ax.set_xlabel("minutes into the window")

ax.set_ylabel("price (Rs)")

ax.legend(loc="best", framealpha=0.9)

fig.tight_layout()

out = Path(__file__).with_suffix(".png")

plt.savefig(out, dpi=110, bbox_inches="tight")

print(f"{len(close)} bars, {int(up.sum())} buy and {int(dn.sum())} exit signals "

f"({close.index[0]:%d-%b %H:%M} to {close.index[-1]:%d-%b %H:%M}). Saved {out.name}")375 bars, 10 buy and 11 exit signals (25-Jun 09:15 to 25-Jun 15:29). Saved 02_signal_chart.png

Across a single 375-bar session on 25 June the raw crossover fired ten buy signals and eleven exits - twenty-one round-trip decisions in one day on one symbol. Lay a realistic cost on each of those flips and the strategy is almost certainly underwater before any edge appears. That gap between the clean signal on the chart and the bruising arithmetic of trading it is the entire reason Module D exists. The loop is the easy part; making it survive contact with spreads, latency, queue position and risk limits is the hard part, and it is what separates a backtest from a business.

We now have the universal skeleton. Next we sharpen it: Chapter 30 sets the same loop spinning at three very different speeds - high-frequency, intraday algo, and systematic - and asks the honest question of where a retail quant can actually compete, and where the laws of latency say you simply cannot.